Johnson Matthey, down 10.5%, in its preliminary results for the year ended 31 March 2022, announced that revenues climbed to £16,025.0m from £15,435.0m recorded in the previous year. Profit before tax narrowed to £195.0m from £224.0m. The board intends to propose a final ordinary dividend of 55.0p.

Kier Group, up 4.3%, in its trading update, announced that the group performed well and in line with the Board’s expectations, in the period from 1 January to 30 April 2022, despite ongoing inflationary pressures.

Marshall Motor, up 0.5%, announced that Group Chief Executive Officer, Daksh Gupta has resigned from his position, with immediate effect.

GRC International Group, unchanged at 26.5p, announced that it has entered into a two-year Payment Card Industry (PCI) security testing contract with a global provider of managed network solutions. The contract is expected to generate approximately £140,000 over a three-year term.

Peel Hunt reiterated its “Buy” rating on Gaming Realms, down 6.7%.

Hilton Food Group, down 5.4%, in its trading update for the period from 3 January 2022 to date, announced that its trading performance has been in line with the management’s expectations, with sales ahead of last year. Whilst the outlook for the year remains challenging, with the impact of higher input prices potentially reducing volume, it expects to make further progress during the year ahead. Further, the company expects to release its results for the 28 weeks ended 17th July 2022 on 15 September 2022.

Aferian, down 0.7%, announced that it has launched 24iQ, an advanced new personalisation and content recommendations service in its 24i business.

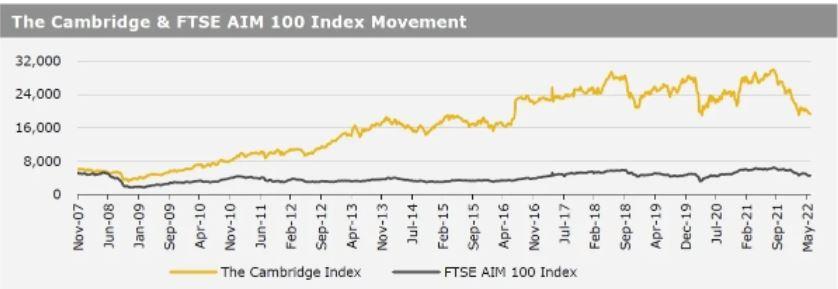

UK markets ended higher last week, helped by gains in banking and retail sector stocks. On the data front, the Rightmove house price index advanced in May. On the other hand, both, UK’s manufacturing and services PMIs declined to a 15-month low in May, as the cost-of-living crisis lowered demand. Additionally, the nation’s public sector borrowing dropped more than expected in May. In a major development, British Finance Minister Rishi Sunak announced a 25% windfall tax on oil and gas companies alongside a £15.0b ($18.9b) support package to help households tackle the cost-of-living crisis. The FTSE 100 index advanced 2.6% to settle at 7,585.5, while the FTSE AIM 100 index rose 1.5% to close at 4,622.8. Also, the FTSE techMARK 100 index gained 2.1% to end at 6,161.6.

US markets ended higher in the previous week, after the US FOMC meeting minutes indicated that the central bank would be flexible with interest rate hikes. On the macro front, the US weekly jobless claims dropped in the week ended 20 May 2022, amid strong demand for workers. Meanwhile, the US economy shrank slightly more than initially estimated in the first quarter of 2022, while the nation’s US durable goods orders rose less than expected in April. Additionally, the US new homes sales declined in April, amid rising prices and higher mortgage rates, while pending home sales fell to 2-year low level in April. Moreover, the US Michigan consumer sentiment index dropped to a 10-year low in May. Separately, the US Federal Reserve hinted at multiple 50-basis-point rate hikes at next couple of meetings and signalled the possibility of a pause in its interest-rate hiking cycle later in 2022. The DJIA index rose 6.2% to end at 33,213.0, while the NASDAQ index gained 6.8% to close at 12,131.1.