Johnson Matthey, down 5.2%, announced that it is planning to shut down its battery materials business, as the firm has been unable to find a buyer for the unit.

Frontier Developments, down 20.8%, in its interim results, announced that revenues rose to £49.12m from £36.91m recorded in the same period previous year.

Xaar, up 7.4%, in its trading update, announced that revenue for the year is expected to be approximately £59m, representing an increase of 23% relative to 2020.

Quixant, up 3.5%, in its trading update, announced that it expects to report full year revenue of $87.1m, ahead of market expectations and driven by strong demand for its products. Also, the group expects to report its full year results for 2021 on 5 April 2022.

Quartix Technologies, up 2.6%, in its trading update, announced that it expects revenue and free cash flow to be in line with market forecasts at £25.6m and £3.8m, respectively. Further, the company expects to release its results for the year ended 31 December 2021 on 1 March 2022.

Cambridge Cognition, up 2.4%, announced that it has won contracts worth £700,000 for two clinical trials by a top 20 pharmaceutical company to assess the pro-cognitive effects of a new drug in schizophrenia.

IQGeo Group, up 0.8%, announced that one of its existing major US telecom customer has signed a new contract for IQGeo's mobile capabilities to support field construction activities.

Science Group, up 0.7%, in its trading update, announced that it has traded strongly during 2021. As a result, it expects to report revenue in excess of £80m and adjusted operating profit to be in the order of £16m, an increase of over 45%.

CyanConnode, down 9.2%, in its trading update for the nine-month period ended 31 December 2021, announced that it has achieved a record turnover of £6.8m and cash collection of £5.9m during the financial year.

SDI Group, down 7.9%, announced that Chief Financial Officer, Jon Abell, intends to step down from the Board.

Bango, down 5.8%, in its trading update, announced that its revenue climbed by 32%, ahead of the board’s expectations, driven by new customer wins. Further, Bango expects to release its 2021 full year results on 8 March 2022.

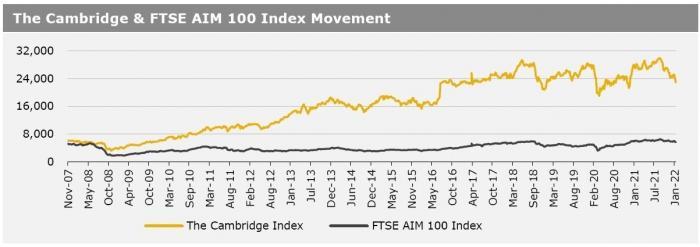

UK markets ended mostly lower last week, on Omicron worries. On the data front, UK’s economic growth rebounded to its pre-pandemic level for the first time in November, partly driven by an unexpected surge in early Christmas shopping. Moreover, Britain’s industrial output climbed in November following two consecutive months of negative growth, while the nation’s manufacturing production rose more than expected in the same month. Additionally, the BRC retail sales climbed in December, while visible trade deficit narrowed in November. The FTSE techMARK 100 index lost 1.8% to end at 6,679.7, while the FTSE AIM 100 index fell 3.3% to close at 5,610.6. Meanwhile, the FTSE 100 index advanced 0.8% to settle at 7,543.0.

US markets ended lower in the previous week, amid concerns over faster interest rate hikes by the Federal Reserve. On the macro front, the US retail sales declined in December, as higher prices induced consumers to spend less, while the nation’s consumer sentiment index dropped to a 10-year low in January, on inflation and Omicron worries. Additionally, the US weekly jobless claims rose to an eight-week high in the week ended 7 January 2022, reflecting an increase in layoffs due to surging Covid cases. Meanwhile, the US consumer prices grew at its fastest pace in nearly 40 years in December, driven by increase in rental accommodation and higher used car prices. The DJIA index fell 0.9% to end at 3,5911.8, while the NASDAQ index lost 0.3% to close at 14,893.8.