AVEVA Group, up 9.9%, in its final results for the year ended 31 March 2022, announced that revenues climbed to £1,185.3m from £820.4m recorded in the last year. The company proposed a final dividend of 24.5p per share (FY21: 23.5p).

Netcall, up 26.7%, announced that it has signed a multi-year contract for the Liberty platform with a S&P 500 international financial services firm. The revenue for the initial three-year cloud subscription period is $19m and is expected to generate similar margins to Netcall's overall group margin.

1Spatial, up 7.4%, announced that it has entered into a two-year contract worth £0.9m with High Speed Two (HS2), the company responsible for developing the UK's new high speed rail network, to build a data validation gateway.

LPA Group, up 3.4%, announced that Chief Financial Officer and Company Secretary, Chris Buckenham would resign from the board, with effect from 31 August 2022.

CyanConnode, down 7.8%, announced that it has appointed Cenkos Securities Plc (Cenkos) as its Nominated Adviser and Joint Broker on 27 April 2022.

Oracle Power, down 6.2%, announced that it has achieved positive metallurgical results from the first of three samples from its 100% owned Northern Zone Gold Project, located in Western Australia. The results showed that good gold recoveries can be achieved within six hours of 83.3%, and up to 90.4% gold recovery over 72 hours.

Xaar, unchanged at 215.0p, announced that it has selected Break as its UK charity partner for the next three years, pledging to match all funds raised up to a sum of £20,000 per year.

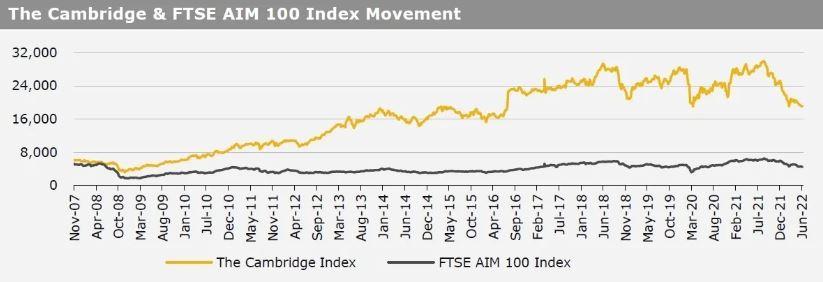

UK markets ended lower last week, on worries over rising inflation and slowing economic growth. On the data front, UK’s services PMI fell in May, hitting its lowest level since February 2021, while the nation’s BRC like-for-like retail sales dropped in May, as consumers cut spending amid surging inflation. Additionally, Britain’s construction PMI declined to a 4-month low in May, while the nation’s housing market showed signs of a slowdown in May. Meanwhile, UK’s Halifax house prices climbed in May. Separately, the OECD warned that Britain is on the brink of recession and would be the worst performing economy with zero growth in 2023. The FTSE 100 index declined 2.9% to settle at 7,317.5, while the FTSE AIM 100 index fell 2.9% to close at 4,505.3. Also, the FTSE techMARK 100 index lost 2.7% to end at 5,905.0.

US markets ended lower in the previous week, as US consumer prices accelerated to a 40-year high. On the macro front, the US consumer price index jumped more than expected in May, strengthening expectations for aggressive rate hikes by the US Federal Reserve. Moreover, the US weekly jobless claims rose to a 5-month high level in the week ended 3 June 2022, while the nation’s consumer sentiment index fell to a record low in May, amid persistent concerns over rising inflation. Meanwhile, the US trade deficit narrowed in April, driven by rise in exports. The DJIA index fell 4.6% to end at 31,392.8, while the NASDAQ index lost 5.6% to close at 11,340.0.