Darktrace, up 1.6%, announced that it has entered into a partnership with Garland Technology to help businesses protect complex industrial environments.

Tristel, up 11.9%, announced that it has received approval from Health Canada for use of Tristel ULT as a Class II Medical Device for endocavity ultrasound probes and skin surface transducers.

Netcall, up 8.5%, in its trading update for the six months ended 31 December 2023, announced that it has witnessed good trading performance in H1 FY24 with results expected to be in line with management expectations. It expects revenue to rise by 8% to £18.9m (H1 FY23: £17.5m) with adjusted EBITDA growth of 9% to £4.8m (H1 FY23: £4.4m).

LPA Group, up 1.2%, in its final results for the year ended 30 September 2023, announced that revenues rose to £21.71m from £19.33m recorded in the previous year. Profit before tax narrowed to £0.76m from £1.07m. The company has proposed a final dividend of 1p per ordinary share of 10p each for the year ended 30 September 2023, payable on 12 April 2024.

SDI Group, down 17.3%, announced the appointment of Stephen Brown as its new CEO, with effect from 19 January 2024, following the resignation of Mike Creedon as CEO and as a director of the company.

Gaming Realms, down 3.0%, announced the launch of its latest branded slot Slingo Hot Roll, under license from King Show Games, including an engaging bonus round where rolling two dice can offer big rewards.

Oracle Power, unchanged at 0.03p, today, in its update, on the farm-in by Riversgold Ltd (Riversgold) on the Northern Zone Intrusive Hosted Gold Project, said Programme of Work (PoW) has been approved by Australia's Department of Energy, Mines, Industry Regulation and Safety (DEMIRS) for drilling. The company expects its planned Reverse Circulate drilling campaign to move the project forward towards a maiden Mineral Resource Estimate in 2024.

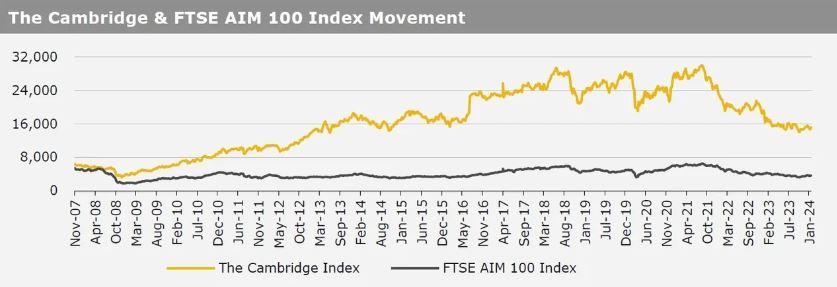

UK markets closed higher last week, following upbeat domestic economic data. On the data front, UK’s manufacturing PMI climbed to a nine-month high in January, while the nation’s services sector advanced to an eight-month high in January, indicating renewed momentum in the economic growth. Additionally, the GfK consumer confidence index rose to a 2-year high in January, while the nation’s public sector net borrowing declined to its lowest level since 2019 in December. The FTSE 100 index advanced 2.3% to settle at 7,635.1, while the FTSE AIM 100 index rose 2.8% to close at 3,638.1. Additionally, the FTSE techMARK 100 index gained 2.5% to end at 6,828.9.

US markets ended higher in the previous week, as a series of positive US economic data eased concerns over recession. On the macro front, the US annualised gross domestic product grew more than anticipated in 4Q23, amid strong consumer spending. Additionally, the US manufacturing PMI rose to a 15-month high in January, while the nation’s services PMI advanced to its highest level since June 2023 in January. Moreover, the US new home sales advanced in December, amid decline in mortgage rates, while the nation’s pending home sales increased in December. On the flipside, the US durable goods orders unexpectedly remained flat in December, driven by lower transportation equipment orders, while the nation’s Richmond Fed manufacturing index unexpectedly fell in January. The DJIA index rose 0.6% to end at 38,109.4, while the NASDAQ index gained 0.9% to close at 15,455.4.