Darktrace, up 10.0%, announced that it has entered into a partnership agreement with HackerOne to combine Darktrace Prevent/Attack Surface Management technology with the continuous security assessment capabilities of the HackerOne platform.

Gaming Realms, up 18.6%, announced that it would release its interim results for the six months ended 30 June 2022 on 20 September 2022.

IQGeo Group, up 4.3%, announced that it has acquired Comsof for around €13.0m. Today, the company announced that it has successfully raised around £3.5m, via a placing of ordinary shares of 2.0p each in the company and a direct subscription of ordinary shares by the Directors of the company and those associated with them each at a price of 125.0p per new ordinary share. The net proceeds of the fundraising will be used in part to fund the acquisition and related transaction expenses, as well as provide further working capital for the group going forward.

Aferian, up 0.7%, announced that it would release its interim results for the six months ended 31 May 2022 on 23 August 2022.

Kier Group, up 0.1%, announced that it has won a bid for the development of the new Velindre Cancer Centre in Cardiff. Separately, the company announced that it has recently partnered with the Ocean Conservation Trust (OCT) on a design and engineering competition to work collaboratively to design a solution that protects seagrass beds.

Checkit, down 19.0%, announced that its annual recurring revenue growth (ARR) was in line with market estimates in 1H FY23, despite a challenging macroeconomic environment. Additionally, its recurring revenue stood at 82% of total revenue for the first half of the year, whereas non-recurring revenue declined as expected. As at 31 July 2022, cash balance stood at £19.5m. Additionally, its interim results would be released on 15 September 2022.

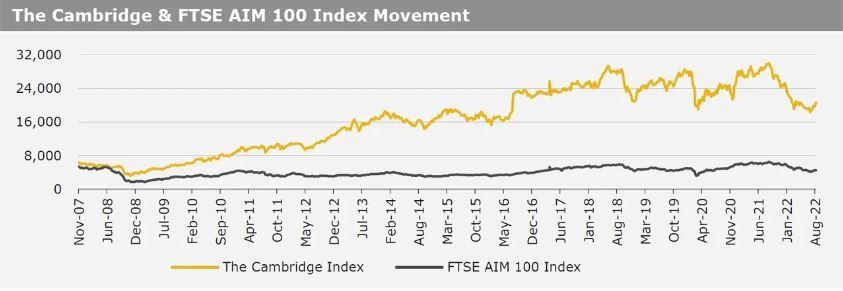

UK markets closed higher last week, amid weakness in the British Pound. On the data front, UK’s BRC retail sales rebounded in July, while the RICS housing prices rose in July. Meanwhile, UK’s economy contracted in 2Q 2022, as households cut spending amid rising inflation and higher interest rates. Additionally, the nation’s goods trade deficit widened in June, amid soaring energy costs. Meanwhile, UK’s industrial production dropped in June, while manufacturing production fell in the same month. The FTSE 100 index advanced 0.8% to settle at 7,500.9, while the FTSE AIM 100 index rose 1.2% to close at 4,512.9. Meanwhile, the FTSE techMARK 100 index added 2.8% to end at 6,201.3.

US markets ended higher in the previous week, after US inflation slowed in July fuelling hopes that the Federal Reserve will become less aggressive on interest rates hikes. On the data front, the US consumer price inflation slowed in July, due to slump in energy prices, while the nation’s producer price index declined for first time since April 2020 in July. Additionally, the US weekly initial jobless claims climbed to a nine-month high in the week ended 5 August 2022, indicating further softening in the labour market. Meanwhile, the US Michigan consumer sentiment index rose to a three-month high in August. The DJIA index rose 2.9% to end at 33,761.1, while the NASDAQ index gained 3.1% to close at 13,047.2.