DS Smith, up 4.9%, announced that it has partnered with Versuni to produce and deliver 100% recycled and recyclable packaging solutions.

SDI Group, up 24.5%, today, announced that it has acquired Peak Sensors Holdings Limited (Peak Sensors or Peak), a UK manufacturer of temperature sensors for a consideration of around £2.4m.

CyanConnode Holdings, up 8.1%, announced that it has received a Letter of Award (LOA) for a follow-on smart metering deployment in the Middle East and North Africa (MENA) region. Under the LOA, the company would supply cellular hubs, with a capacity to connect 1.41m devices. Delivery of the first 7,000 hubs is expected to complete by early November 2023, with the full contract expected to be delivered over the next 12 months.

Xaar, up 1.1%, announced that it has appointed Jacqueline Sutton MBE as Non-Executive Director, with effect from 1 November 2023. She would also serve as a member of the Audit, Remuneration and Nomination Committees. Meanwhile, Chris Morgan would step down as a Non-Executive Director of the Company on 30 November 2023.

Sareum Holdings, down 3.8%, announced that the Japan Patent Office has issued a Notice of Allowance for a patent relating to SDC-1801, the Company's lead TYK2/JAK1 kinase inhibitor. The company anticipates that the patent would be granted in the near future, subject to certain formalities being completed.

Gaming Realms, down 3.1%, announced that it has entered into a partnership with Greentube’s Admiral Casino to strengthen its presence in Europe’s largest online gambling market.

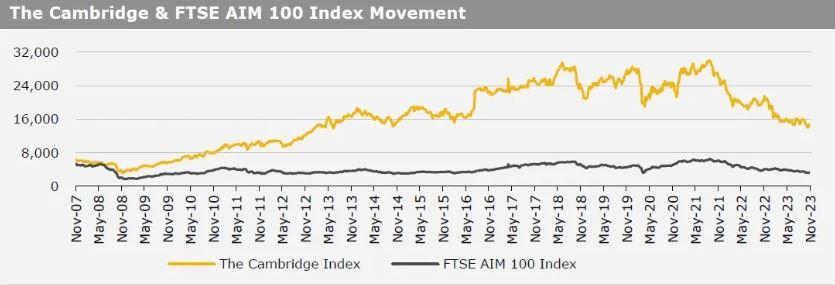

UK markets ended higher last week, amid optimism that the global monetary tightening cycle is nearing its end. On the macro front, UK’s Nationwide housing prices unexpectedly climbed in October, while the nation’s services PMI unexpectedly rebounded in October. Meanwhile, UK’s manufacturing PMI rose less than expected in October, while the nation’s BRC shop price index advanced at its slowest annual pace in more than a year in September. Separately, the Bank of England (BoE) kept its key interest rate steady at 5.25%, for the second time in a row and pledged to keep the policy restrictive for sufficiently long to bring inflation back to the target sustainably. The FTSE 100 index advanced 1.7% to settle at 7,417.7, while the FTSE AIM 100 index rose 4.4% to close at 3,335.5. Also, the FTSE techMARK 100 index gained 5.4% to end at 6,103.1.

US markets ended higher in the previous week, amid hopes that the Federal Reserve (Fed) is done with its interest rate hiking campaign. On the data front, the US factory orders rebounded more than expected in September, following robust demand for electronic products, while the nation’s JOLTS job openings unexpectedly advanced in September. Meanwhile, the US manufacturing PMI contracted in October, amid a drop in new orders, while the US Chicago Purchasing Managers' Index unexpectedly dropped in October. Additionally, the US consumer confidence index eased for a third consecutive month in October, amid persistent worries about inflationary pressures. Moreover, the US private sector employment rose by less than expected in October, while the nation’s initial jobless claims unexpectedly rose in the week ended 27 October 2023. Also, the US nonfarm payrolls rose by less than expected in October. Separately, the US Fed, in its interest rate decision, kept its benchmark interest rate steady at 5.50%, for a second consecutive time. Meanwhile, Fed Chairman, Jerome Powell hinted the US central bank may now be finished with the most aggressive tightening cycle. The DJIA index rose 5.1% to end at 34,061.3, while the NASDAQ index gained 6.6% to close at 13,478.3.