DS Smith, up 15.0%, confirmed that it has received a highly preliminary expression of interest from rival, Mondi plc (Mondi) regarding a combination with the company. The Board of DS Smith understands that Mondi is considering a possible offer for the company although no proposal has been received at this stage.

Kier Group, up 2.2%, announced that it has been selected by the Sussex Partnership NHS Foundation Trust to deliver a new £60m 54-bed acute inpatient mental health hospital in Bexhill as part of its Re-designing Inpatient Services in East Sussex (RIS:ES) Programme.

Oracle Power, unchanged at 0.03p, announced that it has completed a technical and commercial feasibility study (the Study) undertaken by leading international construction engineering company,

China Electric Power Equipment and Technology Co., Ltd. (CET), a wholly owned subsidiary of State Grid Corporation of China (SGCC), Shanghai Investigation, and Design and Research Institute Co. Ltd (SIDRI), relating to the proposed hybrid renewable power plant for the group's green hydrogen and green ammonia project (the Project) in Pakistan.

CyanConnode Holdings, down 11.8%, today, announced that it has secured a significant Letter of Award from its partner, the JST Group, for 101,360 Omnimesh Cellular Modules (CNICs). This LOA builds upon the ongoing deployment and previous orders of Omnimesh RF Modules, Gateways, and 206,735 Omnimesh perpetual software licenses, awarded between 2019 and 2021, for a project in Thailand. Deployment of the Omnimesh CNICs will commence in the first quarter of FY25.

Feedback, down 9.5%, announced that it would release its results for the half year ended 30 November 2023 on 21 February 2024.

Gaming Realms, down 1.7%, in its pre-close trading update for the full year to 31 December 2023, announced that its FY23 revenues are expected to be around £23m and adjusted EBITDA of not less than £10.0m, up 23% and 28% respectively year-on-year, in line with Board's expectations. The company ended the year with £7.5m of net cash. This strong performance has been predominantly driven by content licensing, with growth across all major markets. The company expects to publish its FY23 preliminary results during the week commencing 1 April 2024.

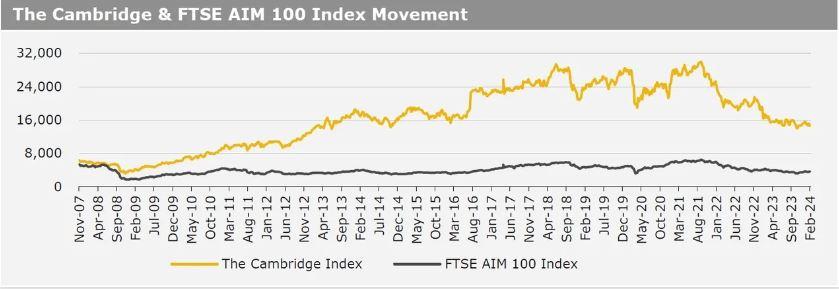

UK markets closed mostly lower last week, amid a rise in British bond yields. On the data front, UK’s services PMI rose at its fastest pace in 8 months in January, while the nation’s construction PMI advanced more than expected in January. Additionally, UK’s BRC like-for-like retail sales climbed in January. Moreover, UK’s Halifax house prices rose for a fourth consecutive month in January, amid lower mortgage rates and the easing of inflationary pressures, while the nation’s RICS housing price balance index advanced more than expected in January. The FTSE 100 index dropped 0.6% to settle at 7,572.6, while the FTSE AIM 100 index fell 1.1% to close at 3,616.6. Meanwhile, the FTSE techMARK 100 index gained 2.3% to end at 6,916.2.

US markets ended higher in the previous week, following robust US corporate earnings reports. On the macro front, the US ISM services PMI climbed at its fastest rate in four months in January, following an increase in new orders. Moreover, the US initial jobless claims dropped for the first time in three weeks in the week ended 02 February 2024, while the nation’s MBA mortgage applications advanced in the same week. Meanwhile, the US trade deficit widened slightly in December. The DJIA index marginally rose to end at 38,671.7, while the NASDAQ index gained 2.3% to close at 15,990.7.