Kier Group, up 7.6%, in its trading update, announced that the first half of the current financial year continued to trade above the prior period and was in line with the Board's expectations.

IQGeo Group, up 19.8%, announced that it expects revenue to exceed £44.2m (2022: £26.6m) representing growth of 66% (organic growth of 56%).

Frontier Developments, up 15.9%, in its interim results, announced that revenues fell to £47.7m from £57.1m recorded in the same period a year ago. Loss before tax stood at £33.1 million, compared to a profit of £6.7m.

Nexteq, up 9.9%, in its trading update, announced that it expects to report full year adjusted profit before tax comfortably ahead of market expectations.

Netcall, up 1.7%, in its AGM statement, announced that robust trading momentum has continued in the first half of FY24, in line with board’s expectations.

Oracle Power, unchanged at 0.03p, in its 4Q 2023 update, announced that it made further progress towards demonstrating the commercial viability of the green hydrogen project in Pakistan.

Bango, down 37.5%, in its trading update, announced that it expects full year revenue of $46.1 million, representing a 62% increase on FY22.

CyanConnode, down 15.2%, announced the appointment of Mr Björn Lindblom as a Non-Executive Director, effective 15 January 2024.

SDI Group, down 2.4%, today, announced the appointment of Stephen Brown as its CEO, with effect from 19 January 2024.

LPA Group, down 1.2%, announced that it would release its preliminary results for the year ended 30 September 2023 on 25 January 2024.

GetBusy, down 0.7%, in its trading update, announced that it continued its positive momentum in line with its strategic goals during 2023, delivering total revenue in line with expectations of £21.1m.

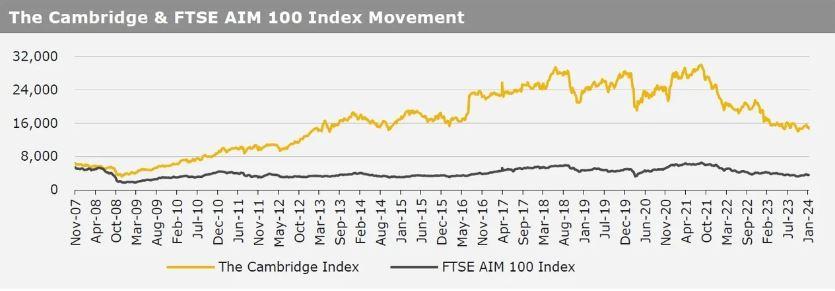

UK markets closed mostly lower last week, following dismal British retail sales data. On the data front, UK’s retail sales dropped at its fastest pace in nearly 3 years in December, stoking concerns over recession. On the flipside, UK’s consumer price index (CPI) accelerated for the first time in 10 months in December, driven by rise in tobacco and air fare prices. Additionally, the RICS house price balance improved in December, while the Rightmove house prices rebounded in January. The FTSE 100 index declined 2.1% to settle at 7,461.9, while the FTSE AIM 100 index fell 1.8% to close at 3,539.1. Meanwhile, the FTSE techMARK 100 index gained 2.5% to end at 6,659.1.

US markets ended higher in the previous week, amid hopes over rate cuts in March 2024. On the macro front, the US retail sales climbed in December, amid rise in motor vehicle and online purchases. Additionally, the US building permits advanced in December, while the nation’s housing market index climbed in January, as mortgage rates fell. Moreover, the US industrial production rose in December, while the nation’s jobless claims unexpectedly dropped to its lowest level since September 2022 in the week ended 12 January 2024. Also, the US Michigan consumer sentiment index climbed to a 2-1/2-year high in January. On the other hand, the US housing starts dropped for the first time in four months in December, while the nation’s existing home sales fell to its lowest level in nearly 30 years in December. The DJIA index rose 0.7% to end at 37,863.8, while the NASDAQ index gained 2.3% to close at 15,311.