Johnson Matthey, down 1.0%, announced that it has successfully completed the lab scale demonstration of its new HyRefine technology for recycling hydrogen fuel cell and electrolyser materials. Separately, the company announced that it has been chosen by Australian green hydrogen and methanol project developer, ABEL Energy to supply two of the key technologies to be deployed for the Bell Bay Powerfuels Project in Northern Tasmania.

Kier Group, up 3.7%, in its AGM trading update, announced that the current financial year FY24 has started well and its trading performance has been in line with the management’s expectations. The order book stood at around £10.5b (30 June 2023: £10.1b) at the end of October. The Group anticipates the usual seasonal working capital outflow during the first half of FY24 which will then reverse in the second half. Further, the company has committed to resume dividend payments in FY24, commencing with an interim dividend.

Frontier Developments, up 3.5%, announced that its real-time strategy game Warhammer Age of Sigmar: Realms of Ruin is available for players on PC via Steam and the Epic Games Store, PlayStation® 5 and Xbox Series X|S for the Deluxe and Ultimate Editions.

CyanConnode Holdings, up 2.4%, announced that its Indian subsidiary, CyanConnode Pvt Ltd, has been recognised as the second fastest-growing UK company in India.

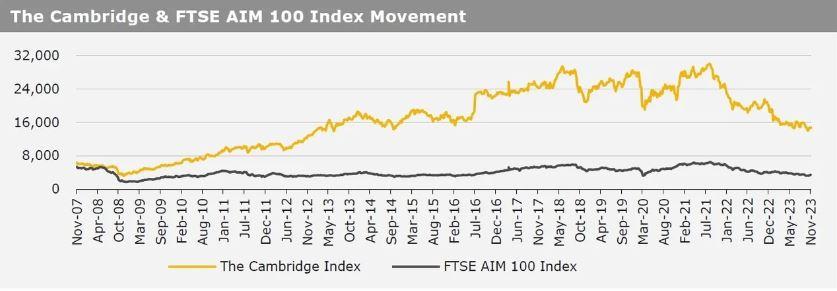

UK markets ended higher last week, as softer-than-expected UK inflation data boosted hopes that the central bank might pause its rate hikes. On the macro front, UK’s consumer price inflation slowed to a 2-year low in October, amid lower household energy prices, while the nation’s retail sales fell to its lowest level since February 2021 in October, amid higher interest rates. Additionally, the Rightmove house price index fell at its fastest pace in five years in November, while the DCLG house price index declined in September. The FTSE 100 index advanced 2.0% to settle at 7,504.3, while the FTSE AIM 100 index rose 2.6% to close at 3,452.4. Also, the FTSE techMARK 100 index gained 1.9% to end at 6,144.3.

US markets ended higher in the previous week, amid prospects that the US Federal Reserve might put an end to its rate hike cycle. On the data front, the US NY Empire State manufacturing index unexpectedly climbed in November. Additionally, the US building permits rebounded in October, while the nation’s housing starts unexpectedly advanced in October. Meanwhile, the US consumer price index advanced less than expected in October, while the nation’s producer price index (PPI) rose less than anticipated in October, amid sharp drop in gasoline prices. Additionally, the US retail sales dropped for the first time in seven months in October, indicating lower consumer spending, while the nation’s initial claims climbed to a 3-month high in the week ended 10 November 2023. Meanwhile, the US industrial production declined in October, while the nation’s housing market index fell in November. The DJIA index rose 1.9% to end at 34,947.3, while the NASDAQ index gained 2.4% to close at 14,125.5.