Darktrace, up 9.1%, announced that it expects Annualised Recurring Revenue at 31st December 2023 of at least $701.7m, representing year-over-year growth of at least 24.3%. Darktrace expects revenue for 1H FY 2024 of at least $329.6m, reflecting year-over-year growth of at least 27.1%.

CyanConnode Holdings, up 7.0%, announced that its subsidiary, CyanConnode Pvt Ltd has secured an order from Montecarlo Limited for 1 million Omnimesh Modules.

Oracle Power, unchanged at 0.03p, provided an update on the farm-in by Riversgold Ltd, on the Northern Zone Intrusive Hosted Gold Project.

IQGeo, down 10.6%, announced that it expects its full year revenue to exceed £44.2m representing 66% growth and 56% organic growth. Separately, the company announced that its fibre planning and design software has been selected by a top 10 US telecom and fibre operator as a part of a first phase technology deployment.

1Spatial, down 1.0%, announced that it has received several multi-year Enterprise contracts in December, strengthening its position across its key geographies.

Quartix Technologies, down 5.2%, in its trading update announced that it expects revenue, profit (adjusted EBITDA) and free cash flow to be around £29.8 million, £4.9 million and £3.1 million, respectively. Moreover, the company expects to publish its results for the year ended 31 December 2023 on 4 March 2024.

Hilton Food Group, down 0.1%, in its full year trading update for the 52 weeks ended 31 December 2023, announced that it expects to report results in line with the Board's expectations, with continued revenue growth and operational progress. Trading during the key festive period was strong, with +3% volume growth in December. On the outlook front, the Board is confident in the outlook for 2024, underpinned by positive recent trading and the Group's strong financial position and cash flows with reduced leverage and comfortable headroom. Additionally, the company expects to publish its preliminary results for the year ending 31 December 2023 on 3rd April 2024.

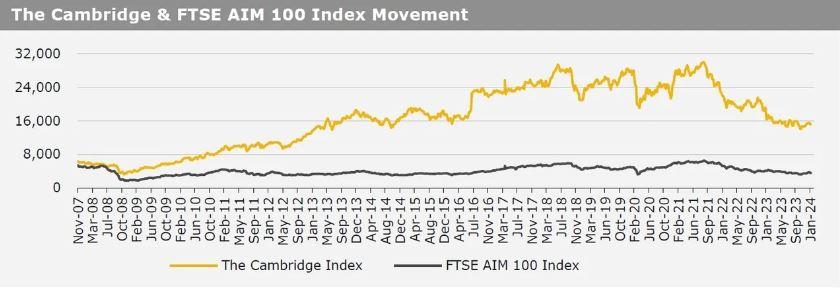

UK markets closed mostly higher last week, as Britain’s GDP grew in November. On the data front, UK’s economic growth rebounded in November, driven by Black Friday sales. Additionally, UK’s manufacturing production climbed in November, while the nation’s industrial production rose as expected in the same month. Further, UK’s goods and trade deficit narrowed in November. The FTSE 100 index fell 0.8% to settle at 7,624.9, while the FTSE AIM 100 index rose 0.05% to close at 3,603.87. Meanwhile, the FTSE techMARK 100 index gained 1.5% to end at 6,496.8.

US markets ended higher in the previous week, ahead of corporate earnings. On the data front, US consumer price index (CPI) accelerated in December, amid rise in housing and healthcare costs, while the nation’s goods and trade deficit narrowed in November, as imports declined. Moreover, the US jobless claims dropped to its lowest level since October in the week ended 05 January 2024. On the other hand, the US producer prices fell for a third straight month in December, amid lower fuel and food prices, while the nation’s budget deficit widened in December. The DJIA index advanced 0.3% to end at 37,592.98, while the NASDAQ index gained 3.1% to close at 14,972.76.