Johnson Matthey, up 1.7%, announced that Bank of America Merrill Lynch upgraded its rating on the company to ‘Buy’ from ‘Underperform’ and raised its target price to 2,000.0p from 1,600.0p.

Dialight, up 1.9%, announced that pursuant to ongoing litigation with its former manufacturing partner, Sanmina Corporation, the court has denied Sanmina's effort to obtain summary judgment and the company now looks forward to seeing it proceed to a satisfactory conclusion.

Xaar, down 29.5%, in its trading update, announced that trading conditions have become more challenging in 2H 2023 due to the wider economic environment. As a result, annual revenues are anticipated to be between £70m and £72m. Moreover, the Board forecasted lower demand during 4Q 2023 that would continue into 2024. The Board remains confident in the medium-term outlook as its opportunities continue to strengthen and further product launches are expected in 2024.

Frontier Developments, down 23.1%, in its business update, announced that its move to diversify its game portfolio during the last five years, including through third-party publishing and new games in 'adjacent genres', has not delivered the anticipated success. Meanwhile, the Company's four CMS games (Planet Coaster, Planet Zoo, Jurassic World Evolution and Jurassic World Evolution 2) continue to perform well and have each achieved over $100m of gross revenue with a combined total of over $500m.

Quartix Technologies, down 3.1%, announced that Non-Executive Directors, Jim Warwick and Russell Jones would step down from the Board. Meanwhile, Alison Seekings would join the Board as Independent Non-Executive Director and Audit Chair.

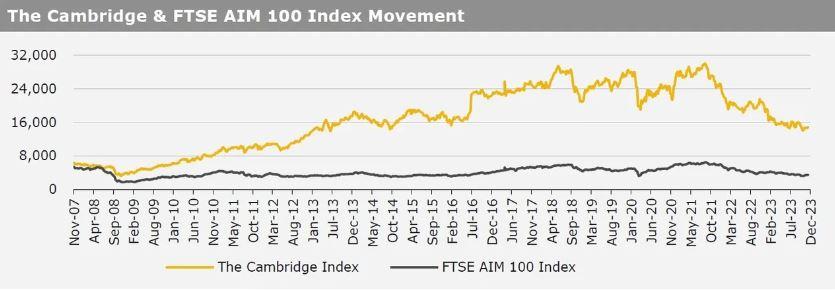

UK markets ended mostly lower last week, after Bank of England Governor, Andrew Bailey highlighted a dim picture of Britain’s economy. On the macro front, UK’s, mortgage approvals rose to a 3-month high level in October, while the nation’s Nationwide housing prices climbed for a third straight month in November. Additionally, UK’s manufacturing PMI advanced in November. The FTSE techMARK 100 index lost 1.3% to end at 6,142.1, while the FTSE AIM 100 index fell 0.2% to close at 3,431.6. Meanwhile, The FTSE 100 index advanced 0.5% to settle at 7,529.4.

US markets ended higher in the previous week, following robust US GDP data. On the data front, the US annualised gross domestic product grew more than expected in 3Q23, amid rise in business investment as well as state and local government spending, while the nations’ consumer confidence index increased in November. Additionally, the US personal income advanced as expected in October, while the nation’s personal spending rose in the same month. Moreover, the Chicago PMI climbed for the first time in over a year in November. Meanwhile, US pending home sales dropped to its lowest level in over twenty years in October, amid higher borrowing costs and prices, while the nation’s new homes sales fell in October. Additionally, the US Richmond Fed manufacturing index unexpectedly declined in November. Separately, the US Federal Reserve’s Beige Book report indicated that the US economic activity slowed from early October through the middle of November. The DJIA index rose 2.4% to end at 36,245.5, while the NASDAQ index gained 0.4% to close at 14,305.0.