Oracle Power remained unchanged at 0.1p, announced the commencement of diamond drilling at the Northern Zone Gold Project in Western Australia, as part of ongoing geotechnical work to support mine planning and finalisation of the Mine Development and Closure Plan. The company stated that conversion of the tenement to a Mining Lease is well advanced and reiterated that development will be funded by MEGA Resources under a 50/50 profit share arrangement.

Checkit up 6.5%, announced that its annual report for the year ended 31 January 2026, together with the notice of its Annual General Meeting, has been posted to shareholders and is available on its website. It said the AGM will be held on 22 May 2026 in London, with proxy votes required to be submitted by 20 May 2026.

Nexteq down 3.6%, announced that its annual report and accounts for the year ended 31 December 2025, together with the notice of its 2026 annual general meeting, have been posted to shareholders and are available on its website. It said the AGM will be held on 22 May 2026 in London.

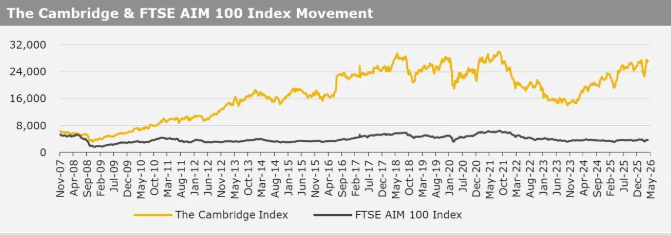

UK markets were mostly higher last week, amid weakness in the British Pound. On the macro front, the UK’s consumer credit demand advanced by more than anticipated in March, while mortgage approvals rose to 4-month high in March. Additionally, the S&P Global Manufacturing PMI advanced to 4-year high in April. Meanwhile, the BRC shop price index rose less than expected in April. Separately, the Bank of England (BoE) kept its key interest rate uncaged at 3.75%. The FTSE 100 index declined 0.1% to settle at 10,363.93, while the FTSE AIM 100 index rose 0.2% to close at 3,745.33. Meanwhile, the FTSE techMARK 100 index gained 1.7% to end at 8,755.15.

US markets ended mixed last week, as concerns over diplomatic impasse between the US & Iran were offset by a series of upbeat corporate earnings reports. On the data front, Initial jobless claims unexpectedly dropped to its lowest level since 1969 in the last week, while the S&P Global Manufacturing PMI rose in April. Moreover, the Richmond Fed manufacturing index advanced more than expected in April. Also, factory orders rose in March and the CB consumer confidence index unexpectedly advanced in April. Meanwhile, gross domestic product (GDP) advanced less than expected in 1Q26, while the Chicago PMI unexpectedly fell in April. Further, goods trade deficit widened in March. While the ISM Manufacturing PMI unexpectedly remained steady in April. Separately, the Federal Reserve (Fed) kept its benchmark interest rate unchanged at 3.75%, for a third consecutive policy meeting. The DJIA index fell 0.6% to end at 48,941.90, while the NASDAQ index gained 0.9% to close at 25,067.80.