Oracle Power, up 20.0%, announced that all objections to its Mining Lease application (M25/389) for the Northern Zone gold project have been settled. The Company is now working with its legal advisers to secure recommendation and grant of the lease by the Department of Mines, Petroleum and Exploration as soon as possible.

Feedback, up 16.3%, announced that it has appointed CFO Emma Oswick (Stuart) to its Board with immediate effect. The Company confirmed no further disclosures are required under AIM Rules. Separately, the company, in its interim results for the period ending 30 November 2025, announced that revenue declined to £0.413m from £0.449m recorded in the same period the previous year. Loss after tax narrowed to £1.742m from £1.878m recorded in the same period the previous year. Cash and cash equivalents stood at £3.82m as of 30 November 2025.

Cambridge Cognition Holdings, up 10.1%, announced that it has partnered with Ivory to commercialise CANTAB Pathway across healthcare and consumer health markets in India. Ivory will deploy the digital cognitive screening tool at scale through its clinical network and consumer platform, expanding early detection of cognitive impairment.

Sareum Holdings, down 16.2%, announced that it has restarted the Phase 2-enabling toxicology programme for SDC-1801, a selective TYK2/JAK1 inhibitor being developed for autoimmune diseases, initially targeting psoriasis. The company has appointed an experienced global CRO to conduct the long-term toxicology studies after discontinuing a previous study in October 2025. The programme is being funded from existing cash resources, with dosing expected to complete by mid-2026 and the full Phase 2-enabling package targeted by year-end 2026. SDC-1801 previously met its primary objectives in Phase 1 trials, demonstrating a once-daily dosing profile with no safety concerns.

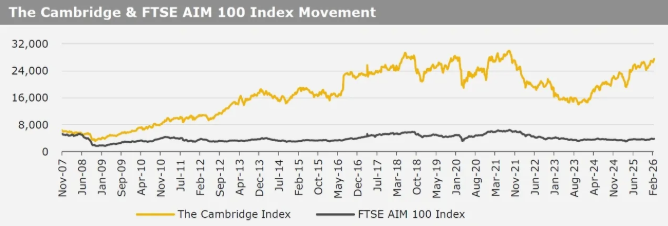

UK market ended higher last week, amid easing concerns over AI disruption. On the macro front, retail sales rose more than expected in January, while UK’s public sector net borrowings reported a surplus in January. Additionally, the S&P Global manufacturing PMI advanced to an 18-month high in February. Meanwhile, UK’s unemployment rate rose in December, while monthly CPI dropped in January. Also, average earnings including bonus advanced less than anticipated in January. Moreover, the S&P Global services PMI dropped to a 2-month low in February. The FTSE 100 index advanced 2.3% to settle at 10,686.9, while the FTSE AIM 100 index rose 0.5% to close at 3,847.4. Meanwhile, the FTSE techMARK 100 index gained 2.4% to end at 8,932.2.

US market ended higher last week, after the US Supreme Court struck down President Donald Trump's global tariffs. On the data front, industrial production unexpectedly climbed in January. Additionally, US weekly jobless claims fell more than expected in the week ended 13 February 2026. Meanwhile, gross domestic product (GDP) rose less than expected in 4Q25. Also, the S&P Global manufacturing PMI unexpectedly declined to a 7-month low in February, while the S&P Global services PMI fell to a 10-month low in February. Moreover, the Michigan consumer sentiment index rose less than anticipated in February. The DJIA index rose 0.3% to end at 49,626.00, while the NASDAQ index gained 1.5% to close at 22,886.10.