Hilton Food Group up 1.3%, announced that its annual report and financial statements for 2025, notice of annual general meeting and proxy form have been submitted to the National Storage Mechanism and are available on its website.

Oracle Power up 20%, announced assay results from 31 drillholes at the Northern Zone Intrusive Hosted Gold Project in Western Australia, marking the completion of the first drilling campaign of 2026, with results indicating continued shallow gold mineralisation and some of the strongest intercepts to date.

Feedback Plc up 14.3%, announced that a central NHS decision on a potential widescale Bleepa rollout, previously expected by 31 March 2026, has been delayed by at least 6–9 months due to internal factors. The company added that existing licences at Queen Victoria Hospital NHS Foundation Trust, with an annualised contract value of £0.50m, have been extended for nine months to December 2026, while broader rollout discussions remain ongoing.

Avingtrans up 12.5%, announced that its Advanced Engineering Systems division is seeing strong growth prospects, supported by increasing demand for nuclear-related applications amid a renewed global focus on energy security, decarbonisation and digital infrastructure. It stated that the division has secured over £10.00m of orders since the start of the year.

GetBusy up 1.4%, announced that it has posted the notice of its annual general meeting to shareholders, with the AGM scheduled to be held on 13 May 2026 at its offices in Cambridgeshire.

1Spatial up 0.7%, announced that the Court has sanctioned the scheme of arrangement for the recommended cash acquisition of 1Spatial Plc by VertiGIS Ltd under Part 26 of the Companies Act 2006, following shareholder approval on 12 March 2026 and satisfaction of conditions announced on 15 April 2026.

Xaar Plc down 0.8%, announced that it has published its annual report and accounts for the year ended 31 December 2025, which includes the notice of its annual general meeting to be held on 27 May 2026.

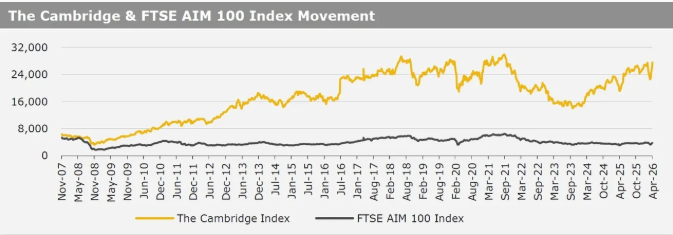

UK markets were higher last week, after Britain’s economy expanded in February. On the macro front, the BRC like-for-like retail sales advanced in March, while gross domestic product (GDP) rose more than expected in March. Additionally, industrial production climbed more than expected in February. Moreover, goods trade deficit widened less than estimated in February. Meanwhile, manufacturing production unexpectedly dropped in February. The FTSE 100 index advanced 0.6% to settle at 10,667.6, while the FTSE AIM 100 index rose 4.0% to close at 3,801.5. Meanwhile, the FTSE techMARK 100 index gained 6.1% to end at 8,764.4.

US markets ended higher last week, amid optimism that the US & Iran could soon reach a deal to end war. On the macro front, initial jobless claims dropped more than estimated in the week ended 10 April 2026, while the Philadelphia Fed manufacturing index unexpectedly advanced in April. Meanwhile, the producer price index rose less than expected in March. Additionally, the NAHP housing price index fell in April. Moreover, US’s industrial production unexpectedly dropped in March. The DJIA index rose 3.2% to end at 49,447.4, while the NASDAQ index gained 6.8% to close at 24,468.5.