AVEVA Group, down 21.1%, announced that at its General Meeting held on 24 November, all the resolutions which were set out in the Notice of General Meeting, were passed as an ordinary resolution through a poll vote.

GRC International Group, up 4.9%, announced that its General Data Protection Regulation (GDPR) European Union (EU) and UK Representative Services for all organisations that need to appoint an EU or UK representative before the Brexit transition period ends on 31 December 2020.

Oracle Power, down 4.2%, announced that further to the company's announcement of 16 November 2020, it has commenced field-based exploration work at the Northern Zone Gold Project, located in the Kalgoorlie region of Western Australia.

Horizon Discovery, down 2.1%, announced that a circular in relation to the Scheme Document, containing, among other things, a letter from the Chairman of Horizon, an explanatory statement pursuant to section 897 of the Companies Act 2006, the full terms and conditions of the Scheme, an expected timetable of principal events, notices of the Court Meeting and General Meeting and details of the action to be taken by Horizon Shareholders, has been published on Horizon's website. Separately, the firm confirmed that, on 27 November 2020, it has 158,361,157 ordinary shares of £0.01 each in issue and admitted to trading on AIM. The International Securities Identification Number (ISIN) for the company's ordinary shares is GB00BK8FL363.

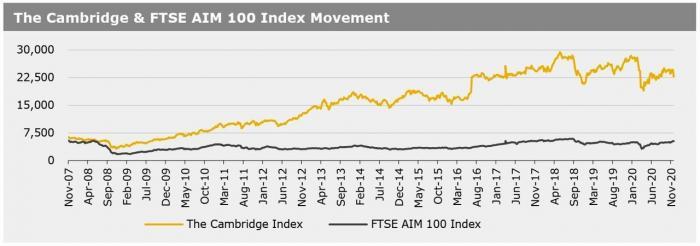

UK markets ended higher last week, buoyed by several positive updates related to the development of a coronavirus vaccine. Meanwhile, the British Finance Minister, Rishi Sunak, during his spending review, warned that budget deficit is expected to climb to its highest level outside wartime and that the UK economy is likely to contract by a historic 11.3% in 2020. On the data front, British manufacturing PMI proved resilient, with output rising, whereas the services PMI dropped to a six-month low in November. The FTSE 100 index advanced 0.3% to settle at 6367.6, while the FTSE AIM 100 index rose 0.7% to close at 5267.4. Also, the FTSE techMARK 100 index gained 0.8% to end at 5981.8.

US markets ended higher in the previous week, following progress on coronavirus vaccines and the formal go-ahead for the US President-elect, Joe Biden’s transition to the White House. Additionally, reports suggested that former Federal Reserve (Fed) Chair, Janet Yellen, is Biden’s pick for Treasury secretary. On the macro front, the second reading of US gross domestic product for 3Q 2020 confirmed rising at a record pace. Further, US business activity in November expanded at its fastest rate in more than five years, pointing to a recovery from the COVID-19 pandemic’s economic damage. Meanwhile, consumer spending came in better-than-expected, but personal income fell in October. A surprise rise in weekly jobless claims to a five-week high added to signs that labour market recovery was stalling, amid a surge in COVID-19 infections. Meanwhile, the Fed’s monetary policy meeting minutes revealed that policymakers discussed how the central bank’s asset purchases could be adjusted to provide more support to markets, with some participants expecting the Fed to eventually lengthen the maturity of the bonds purchased. The DJIA index rose 2.2% to end at 29910.4, while the NASDAQ index climbed 3% to close at 12205.9.