Johnson Matthey, down 7.5%, in its half year results for the six months ended 30 September 2021, announced that revenues jumped to £8,586m compared to £6,979m recorded in the same period last year. The board has declared an interim dividend of 22p per ordinary share, which will be paid on 1 February 2022 to shareholders.

Frontier Developments, down 29.9%, in its trading statement for the 12 months ending 31 May 2022, announced that its best games include Jurassic World Evolution, Planet Zoo, and Planet Coaster, which have performed well. Meanwhile, Elite Dangerous: Odyssey sales have been more muted so far in FY22.

Science Group, unchanged at 435p, announced the completion of an acquisition of Magic Systech Inc – a Taiwan-based company for a net amount of US$2.1m cash.

Kier Group, down 7.9%, announced the completion of the award-winning £20.5m First Light Pavilion at Jodrell Bank Discovery Centre in Macclesfield.

Dialight, down 6.1%, in its trading update for the period from 30 June 2021 to 31 October 2021, announced that its trading performance was good during the period. However, its full-year net debt expectations increased to a range of between £12m and £14m. The company said it would release its full year results on 28 March 2022.

Netcall, down 5.3%, announced that it has posted its annual report and accounts for the financial period ending 30 June 2021, together with the notice of its annual general meeting. The AGM would be held on 16 December 2021 at the offices of Taylor Wessing LLP, 5 New Street Square, London, EC4A 3TW.

Checkit, down 4.1%, announced that it has successfully raised gross proceeds of £21m through the placing of 45,561,020 new ordinary shares at a price of 46p per share.

Marshall Motor, down 3.5%, announced that its largest shareholder, Marshall of Cambridge (Holdings) Limited (MCH) has informed the Board that it is considering a possible sale of its 64% interest holding in the company.

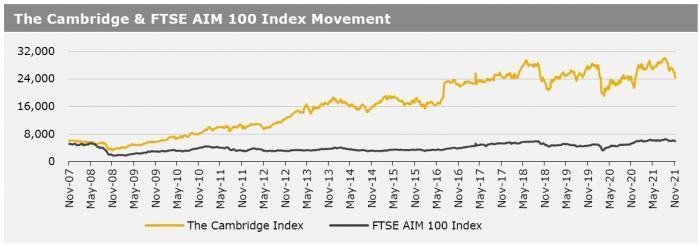

UK markets ended lower last week, amid concerns over the new Omicron variant of Covid-19. On the data front, UK’s manufacturing sector grew to its highest level since 1977 in November, while the nation’s services PMI declined less than expected in November. The FTSE 100 index declined 2.5% to settle at 7044, while the FTSE AIM 100 index fell 3.9% to close at 5827.9. Also, the FTSE techMARK 100 index lost 4.8% to end at 6662.6.

US markets ended lower in the previous week, on fears that the new Covid-19 variant might derail the progress of the economic recovery. On the macro front, the US economy grew less-than-expected in 3Q 2021, while the nation’s durable goods orders unexpectedly declined in October, after a decrease in demand for transportation equipment. Additionally, the US consumer confidence fell in November, amid surging inflation, while new homes sales climbed less-than-expected in October, due to rising house prices.

Meanwhile, the US weekly jobless claims dropped at its lowest level since 1969 in the week ended 19 November 2021, while existing home sales unexpectedly rose at its highest level in nine months in October, reflecting a healthy demand due to low mortgage rates. Also, US consumer spending rebounded in October. In major news, US President Joe Biden has re-nominated Jerome Powell as the Chairman of Federal Reserve for a second four-year term. The DJIA index fell 2.0% to end at 34899.3, while the NASDAQ index lost 3.5% to close at 15491.7.