AVEVA Group, up 0.4%, announced that it has now won all antitrust and regulatory clearances required ahead of completion of the acquisition of OSIsoft.

Johnson Matthey, up 3.8%, announced that it is a partner of the INITIATE (Innovative industrial transformation of the steel and chemical industries of Europe) project consortium which will investigate the potential of a novel synergetic and circular process that transforms residual carbon-rich gas into resources.

Frontier Developments, up 18.2%, stated that it has revealed “The Sphere of Combat”, the third in the series of Elite Dangerous: Odyssey Developer Diaries.

Sareum, up 42.3%, announced that a multi-centre analysis of DNA samples from patients with severe forms of COVID-19 has identified TYK2 as a key causative genetic mechanism and a potential target for therapy. Separately, the firm announced that it has managed to adapt well to the new working conditions and constraints imposed by the COVID-19 pandemic.

Netcall, up 13.6%, announced that a strong momentum continued in the first half of FY21, with trading in line with the Board’s expectation.

Kier Group PLC, up 10.9%. The company will issue a trading statement for the first six months of its FY2021 on 19 January 2021.

GRC International Group, up 6.8%, announced that half year revenue fell to £5.41m from £7.10m.

Tristel, up 4.9%, announced that it expects unaudited first half pre-tax profit to increase by 10%.

CyanConnode, up 2.2%, in its interim results for the period ended 30 September 2020, announced that its revenue rose to £1.50m from £1.01m recorded in the same period previous year.

Oracle Power, down 4.3%, stated that it has welcomed the comments made by Pakistan Prime Minister, Mr Imran Khan, who outlined the Pakistan Government's strong support for developing its coal reserves for coal to liquids and coal to gas projects.

IQGeo Group, down 1.8%, stated that admission of 923,294 initial consideration shares together with the new ordinary shares, would become effective at 8am on 21 December 2020.

Horizon Discovery Group, down 0.3%, referred to an earlier announcement relating to the Boards of Horizon and PerkinElmer stating that they had reached agreement on the terms of a recommended cash acquisition whereby the entire issued and to be issued share capital of Horizon would be acquired by PerkinElmer UK.

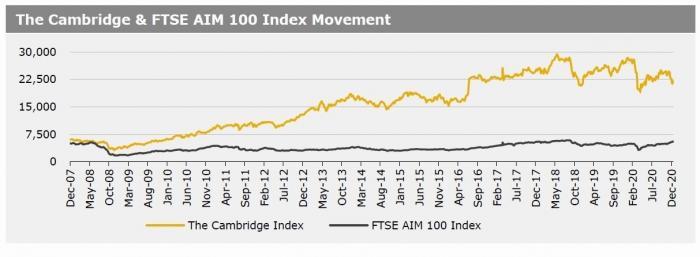

UK markets ended mostly higher last week, with investors hoping that the UK and the European Union would reach a post-Brexit trade deal soon. Meanwhile, UK Chancellor, Rishi Sunak, announced that the government's furlough scheme was being extended to the end of April. On the data front, British inflation slowed on a yearly basis in November. The nation’s unemployment rate rose to its highest level since 2016 in the three months to October. Separately, the Bank of England left its monetary policy unchanged and stated that it was ready to tolerate an inflation spike in the event of a trade deal not being reached. The FTSE 100 index slid 0.3% to settle at 6529.2, whereas the FTSE AIM 100 index rose 3.6% to close at 5598.3. Also, the FTSE techMARK 100 index climbed 2.1% to end at 6250.

US markets ended higher in the previous week, as US lawmakers neared a deal on $900b Covid-19 relief bill. Adding to the positive sentiment, the US Federal Reserve pledged to keep its interest rates at near-zero until the economy recovers. On the data front, new applications for the US unemployment benefits rose to a 3-month high last week, pointing to rising layoffs. Further, US retail sales fell more than expected in November, as consumer spending remained constrained. Meanwhile, the pace of building permit applications reached a 14-year high in November. The DJIA index rose 0.4% to end at 30179.1, while the NASDAQ index gained 3.1% to close at 12755.6.