Kier Group, up 1.6%, announced that it has been appointed by UK's Government Property Agency (GPA) to design and develop the new hub at the Darlington Economic Campus (DEC) in the country.

Frontier Developments, up 27.1%, in its FY24 trading update, stated that its expectations for the financial performance in the current financial year have been improved following the excellent reception to Planet Zoo's arrival on console and a good ongoing performance from its other CMS titles. The board currently expects FY24 revenues of at least £85m.

Aferian, unchanged at 7.4p, today, announced that its AGM would be held at the offices of Bryan Cave Leighton Paisner LLP, Governors House, 5 Laurence Pountney Hill, London, EC4R 0BR on 30 May 2024, at 9.00 a.m.

Oracle Power, unchanged at 0.03p, today, announced the launch of the Grid Interconnection Study for its proposed 1.3GW renewable power plant in Jhimpir, Sindh Province, Pakistan.

Cambridge Cognition Holdings, down 6.7%, in its preliminary unaudited results for the year ended 31 December 2023, announced that revenues rose to £13.52m from £12.61m recorded in the previous year. Loss before tax widened to £3.46m from £0.62m. Cash balance stood at £3.2m as of 31 December 2023 (31 December 2022: £8.3m). Moreover, the company has recently broadened its board by appointing two additional Non-Executive Directors, Nick Rogers and Stuart Gall, post period-end. Meanwhile, Chief Financial Officer (CFO), Stephen Symonds would step down from his role by 30 September 2024 to join an unrelated business.

GetBusy, unchanged at 66.5p, announced that its AGM would be held at the company's offices at The Works, Unity Campus, Pampisford, Cambridgeshire, CB22 3FT at 10.30am BST on 21 May 2024.

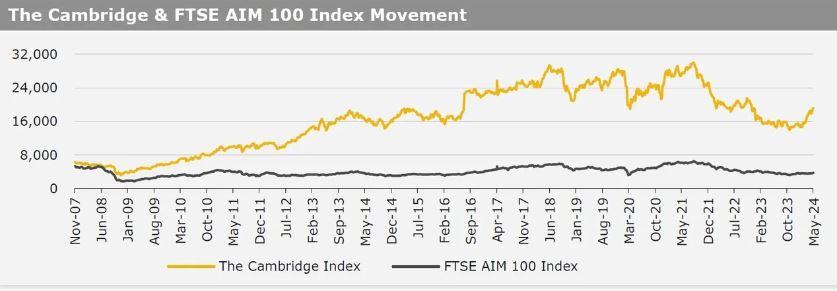

UK markets ended higher last week, amid hopes of early interest rate cuts by the Bank of England (BoE). On the data front, UK’s services PMI rose for the sixth consecutive month in April, while the nation’s manufacturing PMI declined less than expected in April. Additionally, UK’s Mortgage approvals advanced to an 18-month high in March. Meanwhile, UK’s Nationwide housing price index unexpectedly fell in April, while the nation’s BRC shop price index rose to its lowest level since December 2021 in March. The FTSE 100 index advanced 0.9% to settle at 8,213.5, while the FTSE AIM 100 index rose 2.4% to close at 3,724.8. Also, the FTSE techMARK 100 index gained 2.5% to end at 6,885.1.

US markets ended higher in the previous week, amid renewed optimism surrounding rate cuts by the US Federal Reserve (Fed). On the macro front, the US ADP employment climbed more than anticipated in April. Meanwhile, the US ISM manufacturing PMI declined more than expected in April, amid a drop in orders, while the nation’s ISM services PMI fell for the first time since December 2022 in April. Additionally, the US consumer confidence unexpectedly fell in April, while the nation’s Chicago PMI unexpectedly dropped in April. Moreover, the US nonfarm payrolls advanced less than expected in April, while the nation’s unemployment rate unexpectedly rose in April. Also, US JOLTS job openings dropped more than anticipated in March. Separately, the US Federal Reserve (Fed) kept its key interest rate unchanged at 5.50%, as expected. However, the central bank is still leaning towards eventual reductions in borrowing costs. The DJIA index rose 1.1% to end at 38,675.7, while the NASDAQ index gained 1.4% to close at 16,156.3.