Johnson Matthey, up 4%, announced, in its pre-close trading update, that the group’s operating performance is expected to exceed market expectations. Additionally, the company announced that it would be undertaking a strategic review of its health business.

Bango, up 2.3%, announced that India's mobile network operator, Bharti Airtel, has expanded its use of Bango Resale technology to offer Amazon Prime Video Mobile Edition.

Cambridge Cognition Holdings, up 40%, announced that it has secured a contract worth approximately £0.5m with a new pharmaceutical client to provide cognitive assessments in an at-home clinical trial.

CyanConnode Holdings, up 29.1%, announced, in its trading update for the financial year ended 31 March 2021, that revenue during the period stood at £2.5m, exceeding market expectations. Separately, today, the company announced that it has been selected by EESL Energy Solutions LLC, Dubai, (EESL), as technology partner for projects in the Middle East and Africa.

Gaming Realms (former PDX), up 6.1%, announced that it would publish its results for the year ended 31 December 2020 on 27 April 2021.

Marshall Motor Holdings, up 1.7%, announced that Non-Executive Director, Kathy Jenkins, has resigned from the Board with immediate effect.

Quixant, up 0.3%, announced that due to internal process delays at their auditors, KPMG, the 2020 year-end results would now be announced on 14 April 2021. Additionally, the company announced that a live presentation relating to the Group's final results for the year ended 31 December 2020 had been rescheduled to 14 April at 4:45pm BST.

Science Group (former Sagentia Group), which remained unchanged at 310.0p, announced that it has posted its Annual Report and Financial Statements for the year ended 31 December 2020, together with the Notice of Annual General Meeting (AGM). Both documents are available on the Company's website at sciencegroup.com.

UK markets ended mostly higher last week, amid prospects of a planned economic reopening from the coronavirus-led lockdown restrictions starting this week. On the data front, UK’s Markit services PMI rose at its fastest pace since August 2020 in March while the RICS house price balance spiked in February, following an extension of a temporary tax break for property purchases. Additionally, the nation’s Markit construction activity rose to a six-year high in March, buoyed by a restart in delayed hospitality, leisure and office projects.

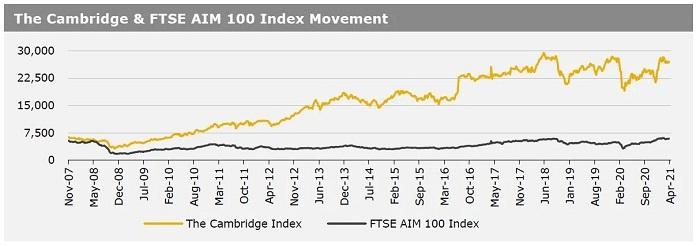

Separately, the International Monetary Fund (IMF) stated that Britain’s economy would grow by 5.3% in 2021, up from its previous forecast of 4.5% and projected a faster post-pandemic growth for the nation compared to the EU and the US. The FTSE 100 index advanced 2.6% to settle at 6915.8, while the FTSE AIM 100 index rose 1.8% to close at 6089.7. Meanwhile, the FTSE techMARK 100 index gained 2.1% to end at 6728.5.

US markets ended higher in the previous week, as upbeat US economic data buoyed prospects for a swift economic recovery. Adding to the positive sentiment, the IMF raised its 2021 forecast for global and US economic growth. The agency expects the US economy to grow 6.4% this year from 5.1%. On the macro front, US services industry activity surged to a record high in March, amid robust growth in new orders while job openings rose to a two-year high in February, helped by speedy rollout of vaccines, trillion-dollar stimulus packages, effective monetary policies. Additionally, the nation’s consumer credit surged by the most since November 2017 in February.

Meanwhile, the Federal Reserve’s latest meeting minutes revealed that rates would remain low until stronger employment and inflation is achieved. The DJIA index rose 2.0% to end at 33800.6, while the NASDAQ index gained 3.1% to close at 13900.2.