Global fintech investments in 2021 totalled $210bn across 5,684 deals – an eye-watering figure that is proof of the sector’s continued strength. With traditional banking institutions also looking to adopt fintech practices in their digital offerings to customers, successful startups in the fintech space now have significant opportunities to impact the ways in which money moves around the world.

While it’s true that countries such as the United States, the United Kingdom and Germany continue to dominate fintech industry rankings such as those compiled by Findexable, 2021 has also seen the significant rise of markets in Africa, South America and South-East Asia. The growth here is significant: African tech investment totalled $350m in 2020. In 2021, individual deals, such as those recorded by Jumia ($326m) have almost equalled that figure.

Such strong showings in markets that have previously remained relatively untapped is fuelling fintechs’ appetite for growth, and leading many to consider these regions for inclusion in their next expansion phases. In one of its ‘Pulse of Fintech’ publications, KPMG identified trends suggesting that investment in traditionally financially under-developed regions, such as Africa, Latin America and the Middle East would continue to grow in 2022. However, in order to be successful, it is important they develop a deep understanding of the specificities of each region, including demographics, financial challenges, and, importantly, financial literacy.

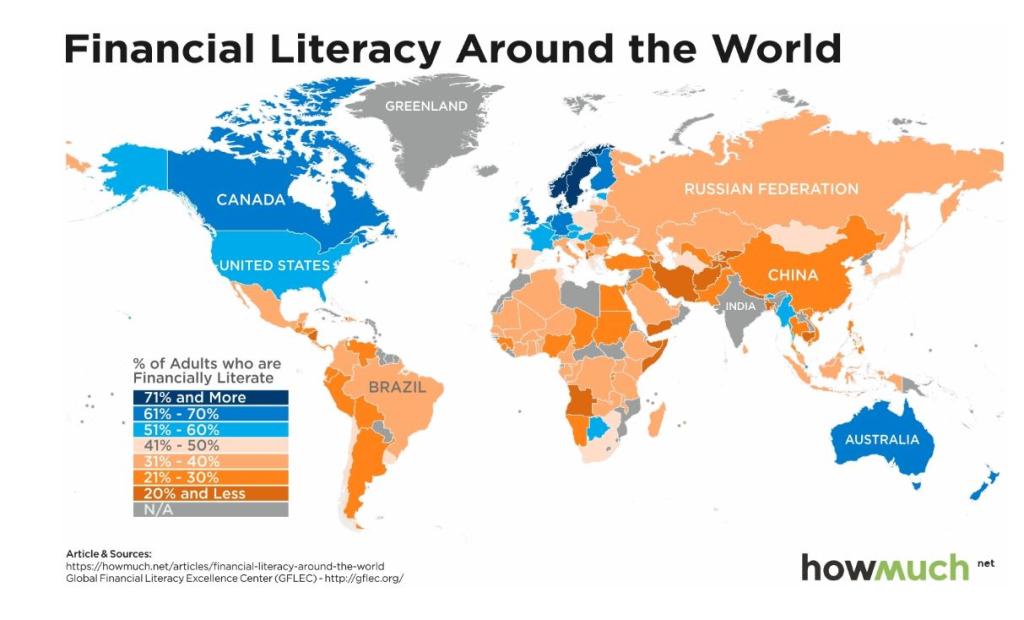

Financial literacy indicates an individual’s ability to make financially sound decisions, with rates varying wildly around the world. Research has shown that regions such as Northern and Western Europe, North America and Oceania are typically the most financially literate, recording a financial literacy rate of between 51% to 71% among adult populations. Conversely, Africa, South America, the Middle East and areas of Asia tend to be less financially literate, recording rates of below 20% in some places, and up to just under 50% in others.

For fintechs, this is an impressive challenge; research has typically shown correlations between lower financial literacy rates and reduced adoption of fintech services. In a paper on the relationship between financial literacy and fintech adoption in Vietnam, published in the Sustainability journal, Thi Anh Nhu Nguyen identifies that “financial literacy has been shown to have a positive relationship with fintech adoption,” and that “if individuals are confident about knowledge themselves, they have a higher propensity to use fintech applications”. Nguyen’s study of Vietnamese markets indicated that it might be this self-perceived knowledge that has a larger effect on fintech adoption than actual financial knowledge. It is possible then, that through the provision of clear, well-explained functionality, fintechs could foster confidence among potential users, and grow their install base, in spite of traditionally low financial literacy rates.

Now, some fintechs are taking it upon themselves to improve global financial literacy. Companies such as World of Money provide online financial lessons and services to help children and young adults become financially literate. Applications like Zogo gamify financial education to encourage users to continue engaging with content and expanding their financial knowledge. It’s hoped that users of companies and applications such as these will go on to make wiser decisions about where to invest their money, and will likely lead to continued growth for the fintech industry as a whole.

For many fintechs, explaining complicated financial concepts and jargon can prove challenging. While increased financial literacy rates across the board could help reduce such challenges in the future, these long-term solutions won’t make a significant difference to fintechs looking to onboard customers now. These companies will need to provide frictionless onboarding alongside continued user education in order to increase their customer base’s financial literacy, as well as foster trust among users.

Applications such as Moneytrans are strong examples of continued user education. An application allowing users to easily transfer money between international markets, Moneytrans requires users to select a destination country and payout method before money can be transferred. The application provides links for users to click on to find out more information on the specified country and the various available payout methods, helping customers to feel confident that they aren’t making mistakes when using the service.

Other applications, such as USA-based Albert, look to connect users with financial advisers that can act as a sounding board for questions users may have regarding investments, savings and day-to-day spending. Albert’s ‘Genius’ services combines financial expertise and advanced technology to help customers decide how to approach their finances, supporting decisions such as whether to buy or lease a car. With strong user bases on both Apple and Android devices, it’s clear that Albert’s approach to user education has been a hit with its audience.

Whichever markets fintechs are looking to target, it’s important that they develop a deep understanding of typical financial literacy in the region, so that they can provide the right levels of onboarding and support. As Nguyen noted in his study of fintech adoption in Vietnam, “perceived utility and perceived user-friendliness are two critical predictors that could affect the users’ intention of accepting technology”. For fintechs, it can be difficult to improve their perceived utility if they are unable to break down and explain their services in ways that their audiences can understand.

In order to educate international users and close the financial literacy gap, fintechs will need to speak with audiences in their language. In traditionally under-developed markets with lower financial literacy, this could mean putting customer education and specific assistance aimed at customer lifestyles at the core of their service offering. This is a practice perhaps best evidenced by Sri Lankan insurance platform Etherisc, which collaborated with Oxfam and insurance company Aon to provide agricultural insurance to paddy farmers.

Oxfam provided on-the-ground education about risks the farmers could expect, while Etherisc built a platform with smart contracts that automated weather-based claims, which in turn reduced Aon’s costs as an insurance provider. The collaboration proved fruitful: approaching customers directly at ground level, The team was able to educate the customers on the specific uses of the fintech that would impact them most. In this way, the service was able to foster trust and improve their financial literacy. Overall, the farmers found that the service was more convenient than previous insurance plans, as they didn’t have to make all claims themselves. This collaborative effort is one of the clearest examples of how thorough education can help fintechs meet success in traditionally under-developed locales.

Alpha CRC is a global provider of Enterprise Localization services, drawing on its international network of in-country subject matter experts to advise fintech clients on their expansion and localization strategies. Enterprise Localization practices ensure that Alpha CRC supports clients from early-stage strategizing to post-localization user experience quality assurance processes.