DS Smith, up 3.4%, announces that pursuant to the Code, Mondi was required either to announce a firm intention to make an offer for DS Smith under Rule 2.7 of the Code or to announce that it does not intend to make an offer. However, DS Smith has requested, and the Panel on Takeovers and Mergers (the Panel) has consented to, a further extension to the deadline until 5.00 p.m. (London time) on 23 April 2024. The deadline may be extended further with the consent of the Panel under Rule 2.6(c) of the Code.

Hilton Food Group, up 2.6%, in its preliminary results for the 52 weeks ended 31 December 2023, announced that revenues rose to £3.99b from £3.85b recorded in the previous year. The Directors have proposed a final dividend of 23.0p (2022: 22.6p) per share, payable on 28 June 2024 to shareholders.

Kier Group down 4.7%, announced that it has been chosen by UK operator Network Rail for lot A1 of the North West & Central Region Control Period 7 (CP7) Framework.

Frontier Developments, up 30.9%, in its trading update, announced that sales across its portfolio have been in line with expectations, with the largest contributions being provided by Frontier's creative management simulation (CMS) games, led by Jurassic World Evolution 2 and Planet Zoo.

Sareum Holdings, up 7.0%, announced the completion of raising gross proceeds of £2.29mn via the issue of, in the aggregate, 22,889,733 new ordinary shares at the placing price of 10p per new ordinary share.

Bango, up 3.4%, today, its full-year results, announced that revenues rose to $46.09m from $28.49m recorded in the previous year.

GetBusy, up 0.8%, announced that it has acquired trade and assets of SmartPath LLC (SmartPath) to boost its product offering into the pricing and small-practice management space in the US market.

Gaming Realms, down 5.8%, in its annual results, announced that revenues rose to £23.4mn from £18.7mn recorded in the previous year. The Board of Directors did not propose a final dividend for the period.

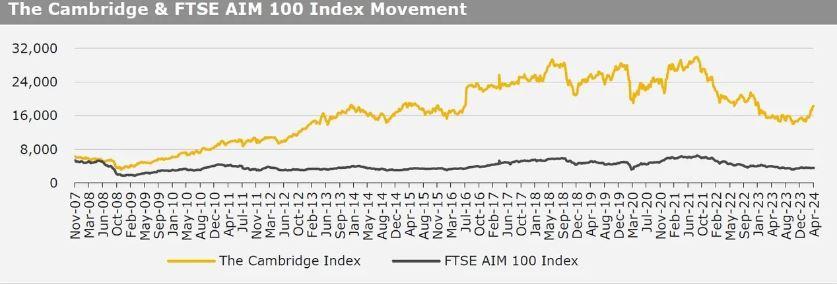

UK markets ended lower last week, as rising geopolitical tensions in the Middle East. On the data front, UK’s services PMI dropped more than anticipated in March. Moreover, UK’s Nationwide housing prices unexpectedly fell in March, while the nation’s Halifax house prices declined for the first time in 6 months in March, amid higher mortgage rates. Also, UK’s BRC shop price index rose at the slowest pace in more than two years in March. Meanwhile, UK’s manufacturing PMI climbed to a 20-month high in March. The FTSE 100 index declined 0.5% to settle at 7,911.2, while the FTSE AIM 100 index fell 0.7% to close at 3,578.4. Also, the FTSE techMARK 100 index lost 1.3% to end at 6,796.3.

US markets ended lower in the previous week, as US Federal Reserve officials indicated that the central bank could delay cutting interest rates. On the macro front, the US ISM services PMI unexpectedly dropped in March, while the nation’s US trade deficit unexpectedly widened in February. Moreover, the US weekly jobless claims rose more than expected in the week ended 29 March 2024. Meanwhile, the US ISM manufacturing PMI rose for the first time in 1-1/2 years in March, amid a sharp rise in production and new orders, while the nation’s factory orders expanded more than expected in February, driven by demand for machinery and commercial aircraft. Additionally, the US ADP employment climbed at its fastest pace since July 2023 in March, while the nation’s JOLTS job openings unexpectedly rose in February. Also, the US nonfarm payrolls climbed more than expected in March, while the nation’s unemployment rate unexpectedly dropped in March. The DJIA index fell 2.3% to end at 38,904, while the NASDAQ index lost 0.8% to close at 16,248.5.