Johnson Matthey, down 1%, announced that it has partnered with Kebotix to explore developing the next generation of coatings for catalytic converters.

Abcam, up 7.1%, announced that it has agreed to acquire BioVision, Inc., a wholly owned subsidiary of Boai NKY Medical Holdings Ltd., for a consideration of $340m.

CyanConnode, up 24.4%, in its audited results for the year ended 31 March 2021, announced that revenues jumped to £6.44m from £2.45m recorded in the previous year. The Directors do not recommend the payment of a dividend (2020: £nil).

Dialight, up 12.1%, in its half year results for the period ended 30 June 2021, announced that revenues climbed to £60.2m from £55.2m recorded in the corresponding period of the last year. The Board is not declaring an interim dividend for 2021 (2020: nil).

Marshall Motor, up 10.3%, in its trading update, announced that continuing underlying profit before tax for 2021 would be not less than £40m. Further, the firm cautioned that high level of uncertainty would remain over the second half of 2021, due to the impact of the COVID-19 pandemic. The Group would publish its interim results for the six months ended 30 June 2021 on 10 August 2021.

Cambridge Cognition, up 4.5%, in its trading update, announced that it has witnessed a strong performance in the first half of 2021, driven by significant growth in revenues. The interim results for the six months ended 30 June 2021 would be announced on 21 September 2021.

Aferian, down 1%, in its unaudited results for the six months ended 31 May 2021, announced that revenues rose to $45.3m from $38m recorded in the same period previous year. The Board has proposed to pay an interim dividend of 1p per share, payable on 2 September 2021.

Netcall, unchanged at 74.5p, today, announced that it has signed a global framework agreement with a leading multinational financial services firm having operations in around 120 countries.

UK markets ended higher last week, following upbeat earnings reports. On the data front, both, the manufacturing and services PMIs in the UK declined in July, driven by labour shortages and supply chain problems, while the construction PMI dropped to its lowest level since February in July, amid shortages of materials and skilled labour. Additionally, UK’s house price inflation slowed at its fastest pace in four months in July, as the end of the temporary stamp duty holiday dampened investor sentiment.

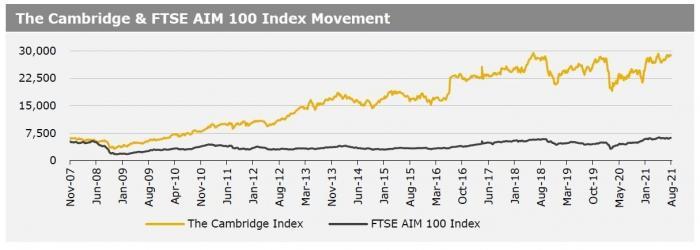

Separately, the Bank of England (BoE) kept its key interest rate unchanged at 0.10% and indicated that inflation could rise to 4% this year, amid rising energy and other goods prices. The FTSE 100 index advanced 1.3% to settle at 7123, while the FTSE AIM 100 index rose 0.8% to close at 6240.2. Also, the FTSE techMARK 100 index gained 3.3% to end at 7223.1.

US markets ended higher in the previous week, as US jobs data came in better-than-expected reflecting momentum in the US economic recovery. On the macro front, the nation’s services sector index jumped to a record high in July, buoyed by the shift in consumer spending to services from goods, while factory orders climbed more than expected in July. Additionally, the US weekly jobless claims dropped for a second consecutive week in the week ended 30 July 2021, while the nation’s non-farm payrolls climbed at its fastest pace in July, despite growing concerns over the coronavirus Delta variant.

Meanwhile, the US manufacturing PMI declined in July, amid ongoing supply-chain problems, while private sector employment rose less-than-expected in the month of July. The DJIA index rose 0.8% to end at 35208.5, while the NASDAQ index gained 1.1% to close at 14835.8.