AVEVA Group, down 0.03%, announced that the scheme document containing the full terms and conditions of the acquisition of the company (excluding AVEVA Shares held by Samos, an indirect wholly owned subsidiary of Schneider Electric) by Bidco, together with the related Forms of Proxy, is being published and sent to its Shareholders.

Abcam, down 7.2%, announced that it intends to cancel the admission of its ordinary shares of nominal value 0.02p each to trading on AIM, with effect from 14 December 2022. However, the company would retain the listing on the Nasdaq Global Select Market under ticker symbol ‘ABCM’.

Cambridge Cognition Holdings, up 8.8%, announced that it has received a contract worth £1.1m with a pharmaceutical company to supply hardware and electronic clinical outcome assessments (eCOA) for a rare blood condition that will take place over the following two years.

Sareum Holdings, up 7.4%, today, in its audited results for the year ended 30 June 2022, announced that it reported nil revenues during the period. Loss before tax widened to £2.6m from £1.7m.

SDI Group, up 2.4%, today, announced the acquisition of Fraser Anti-Static Techniques Limited for an expected total consideration of approximately £13.0m.

Aferian, unchanged at 130.0p, announced that the remaining contingent consideration in relation to the 24i Unit Media A/S acquisition in May 2021 has become payable. Accordingly, the company would pay a final amount of €117,000 of which €26,910 would be paid in cash and the remaining €90,090 would be settled through the issue of 52,769 new ordinary shares of 1.0p each in the capital of the company at the price agreed at the date of the original acquisition of 148p per Ordinary Share.

Oracle Power, unchanged at 0.2p, announced that it has selected thyssenkrupp Uhde to head the technical and financial feasibility study for the green hydrogen and ammonia project being developed by the Company's joint venture company, Oracle Energy Limited.

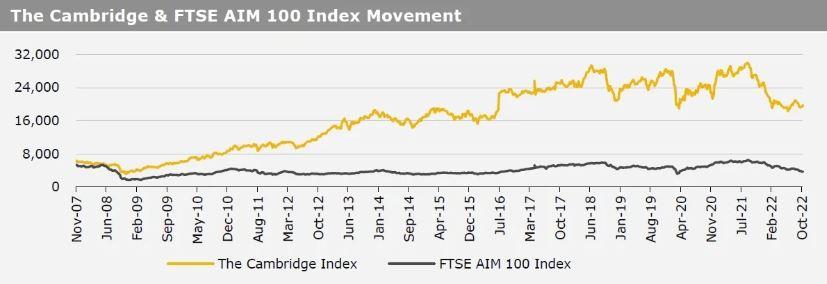

UK markets closed firmer last week, after UK’s new finance minister scrapped almost all planned tax cuts. On the macro front, UK’s consumer price index (CPI) jumped to a 40-year high in September, amid soaring food prices, while the nation’s house price index climbed more than anticipated in September. Additionally, the GfK consumer confidence improved in October. Meanwhile, UK’s retail sales fell for a second consecutive month in September, as cost-of-living pressures hit consumer spending, while the nation’s public sector borrowing jumped in September. The FTSE 100 index advanced 1.6% to settle at 6,969.7, while the FTSE AIM 100 index rose 1.1% to close at 3,728.4. Meanwhile, the FTSE techMARK 100 index gained 1.1% to end at 5,843.0.

US markets ended higher in the previous week, amid hopes that the US Federal Reserve (Fed) would be less aggressive in interest rate hikes. On the data front, the US industrial production rebounded in September, while the nation’s initial jobless claims unexpectedly declined in the week ended 14 October 2022. Moreover, the US building permits rebounded in September. On the contrary, the US housing starts declined in September, amid cooling demand in the housing market, while the nation’s existing home sales dropped to a 10-year low in September, amid higher mortgage rates. Additionally, the NAHB housing market index fell for a tenth straight month in October, as rising interest rates, building material bottlenecks dampened demand for housing, while the nation’s MBA mortgage rates dropped to a 25-year low in the week ended 14 October 2022, amid interest rate hikes. Further, the US NY Empire State manufacturing index declined more than expected in October. The DJIA index rose 4.9% to end at 31,082.6, while the NASDAQ index gained 5.2% to close at 10,859.7.