DS Smith, down 1.6%, announced that it has completed the sale of De Hoop paper mill in Netherlands in a deal worth €50m to De Jong Packaging.

Oracle Power, up 32.8%, announced that it has entered into a non-exclusive co-operation agreement with PowerChina International Group Ltd to jointly develop a 400-MW solar PV-powered green hydrogen production plant in Pakistan. Separately, the firm announced the completion of the first phase of Reverse Circulation (RC) drilling at the Northern Zone Gold Project in Western Australia.

Feedback, up 10.3%, announced that it has signed a Memorandum of Understanding (MoU) with Quest Teleradiology Solutions to develop strategic opportunities for its flagship clinical communications platform, Bleepa.

Marshall Motor, up 4.6%, announced that it has acquired the entire issued share capital of Motorline Holdings Limited (including all of its subsidiaries), for a cash consideration of £64.5m.

Science Group, up 4.5%, in its trading and business update, announced that it has performed well, despite supply shortages. The Board expects further upside in the Group's 2021 profitability forecasts.

1Spatial, up 3.6%, announced that it has won a new multi-year framework agreement by Land and Property Services (LPS) in Northern Ireland, as a key supplier to support the Department of Finance's ongoing programme of digital transformation.

Kier Group, up 1.2%, announced that its annual general meeting will be held at the offices of Linklaters LLP, One Silk Street, London EC2Y 8HQ on 19 November 2021 at 10.00 am.

Tristel, down 13.7%, today in its unaudited preliminary results for the year ended 30 June 2021, announced that revenues dropped to £31m from £31.68m recorded in the previous year. The Board has recommended a final dividend of 3.93p (2020: 3.84p), an increase of 2%.

Quartix Technologies, down 6.6%, in its trading update announced that it anticipates revenue, profit and free cash flow for the year ended 31 December 2021 to be in line with current market forecasts.

CyanConnode, down 6.1%, in its trading update for the six months ended 30 September 2021, announced that its sales turnover stood at £4.10m, 2.7 times higher than the equivalent FY 21 period. Cash and cash equivalents stood at around £1.74m compared to £1m.

UK markets ended higher last week, as Britain’s economy returned to growth in August, as Covid-19 restrictions continued to ease across the country. On the data front, UK’s gross domestic product grew in August, while the nation’s unemployment rate dropped in the three months to August. Additionally, Britain’s, both, industrial and manufacturing production climbed in August. On the contrary, UK’s trade deficit widened in August.

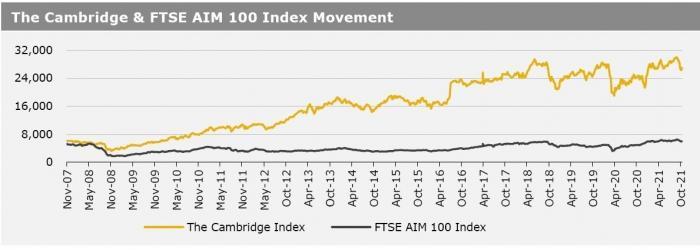

The FTSE 100 index advanced 2.0% to settle at 7234.0, while the FTSE AIM 100 index rose 1.7% to close at 6030.1. Also, the FTSE techMARK 100 index gained 2.1% to end at 7204.6.

US markets ended higher in the previous week, after the US Federal Reserve (Fed) indicated that it would stick to its previously announced taper timeline. On the macro front, the US consumer prices climbed to a 13-year high in September, reflecting higher prices for food, rent, and other goods, while the nation’s weekly jobless claims dropped to its lowest level since March 2020 in the week ended 8 October 2021. Moreover, the US retail sales unexpectedly climbed in September.

Separately, the US FOMC minutes indicated that the central bank could start tapering its asset purchases by $15t in mid-November or mid-December. The DJIA index rose 1.6% to end at 35294.8, while the NASDAQ index climbed 2.2% to close at 14897.3.