AVEVA Group, up 0.1%, announced that Bernstein downgraded the stock to ‘Market Perform’ from ‘Outperform’.

CyanConnode Holdings, up 26.9%, announced that it has received an order for 983,525 Omnimesh Modules, Advanced Metering Infrastructure, Standards-Based Hardware, Omnimesh Head-End Software, Perpetual License, and a Support and Maintenance Contract from Montecarlo Limited.

Checkit, up 21.1%, announced that it has won three contracts in the US which would generate a combined minimum value of approximately $1m over their three-year terms. Of these two are with biopharma companies and the third is with a large resort and casino operator on the West Coast. The company has also received a contract renewal in the UK worth around £2.1m over four years with an integrated energy company to provide real time operations management capabilities to over 300 sites.

Kier Group, up 7.1%, announced that Independent Non-Executive Director, Chris Browne has stepped down from the Board of Norwegian Air Shuttle ASA, with effect from 31 December 2022.

Frontier Developments, up 4.0%, Shore Capital upgraded its rating on the stock to ‘Buy’ from ‘Hold’. Separately, the company, in its trading update for the financial period ending 31 May 2023, announced that it expects revenue for H1 FY23 to be approximately £57m (H1 FY22: £49.1m). Cash balance stood at £42.6m as at 30 November 2022 (31 May 2022: £38.7m). Further, the company would release its interim financial results for H1 FY23 on 19 January 2023.

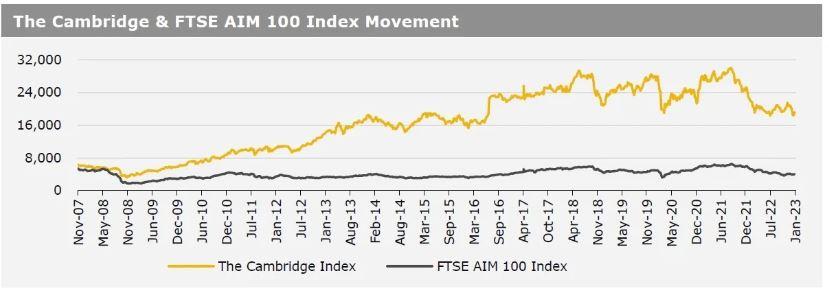

UK markets closed higher last week, following upbeat quarterly corporate earnings reports. On the macro front, UK’s Halifax house prices fell for a fourth straight month in December, amid cost-of-living crisis and higher interest rates, while the nation’s mortgage approvals declined to its lowest level since June 2020 in November, as higher borrowing costs reduced demand for property. Moreover, Britain’s construction PMI declined in December. Further, UK’s manufacturing PMI declined to its lowest level since May 2009 in December while, the nation’s services PMI advanced less than expected in December. Meanwhile, UK’s consumer credit advanced more than forecasted in November, amid surge in food prices. The FTSE 100 index advanced 3.3% to settle at 7,699.5, while the FTSE AIM 100 index rose 2.5% to close at 4,065.4. Meanwhile, the FTSE techMARK 100 index gained 3.2% to end at 6,530.3.

US markets ended higher in the previous week, as slowdown in wage growth signalled signs of cooling inflation. On the data front, the US JOLTS job openings fell less than anticipated in November, while the nation’s initial jobless claims unexpectedly declined to its lowest level in 14 weeks in the week ended 30 December 2022. Additionally, the US private sector employment advanced by more than anticipated in December, while the nation’s nonfarm payrolls climbed in December. Meanwhile, the US ISM manufacturing PMI dropped for a second straight month in December, amid drop in demand, while the nation’s factory orders fell more than estimated in December. Additionally, the ISM services PMI dropped for the first time in more than 2-1/2 years in December. The DJIA index rose 1.5% to end at 33,630.6, while the NASDAQ index gained 1.0% to close at 10,569.3.