Johnson Matthey, up 9.8%, announced that it has inked a multi-year partnership agreement with Plug Power.

Darktrace, down 3.5%, announced a share buyback programme of up to 35m of its ordinary shares.

Kier Group, up 2.3%, announced that it has appointed Louisa Finlay as Chief People Officer and member of the executive committee.

Gaming Realms, up 7.6%, announced in its pre-close trading update for the full year to 31 December 2022, that it expects to report FY22 revenue of approximately £18.7m and adjusted EBITDA of approximately £7.7m. The company expects to report its FY22 preliminary results during the week commencing 3 April 2023.

Oracle Power, up 6.8%, announced in its Q4 update, that Global industry leaders in green ammonia development, thyssenkrupp Uhde, were appointed to carry out the technical and feasibility study for Oracle Energy's flagship Green Hydrogen Project in Pakistan, due be completed in H1 2023.

Science Group, up 2.6%, announced that it has completed the sale of the entire issued share capital of Westek Technology to Roda Computer GmbH for a cash consideration of £0.8m.

SDI Group, up 1.7%, announced the appointment of Louise Early to the Board as an Independent Non-Executive Director, with effect from 1 February 2023 as well as member of the Remuneration, Audit and Nominations Committees.

LPA Group, up 0.7%, announced in its preliminary results for the year ended 30 September 2022, that revenues rose to £19.3m from £18.3m compared to the previous year.

Tristel, down 5.8%, announced that its interim results for the six months ended 31 December 2022 will be published on 20 February 2023.

Cambridge Cognition Holdings, down 4.3%, announced in its trading update for the year ended 31 December 2022, that it expects revenue to rise 25.0% ahead of market expectations to £12.6m (2021: £10.1m.

Quixant, down 0.3%, announced that it has launched its market leading QMAX gaming hardware platform at ICE 2023.

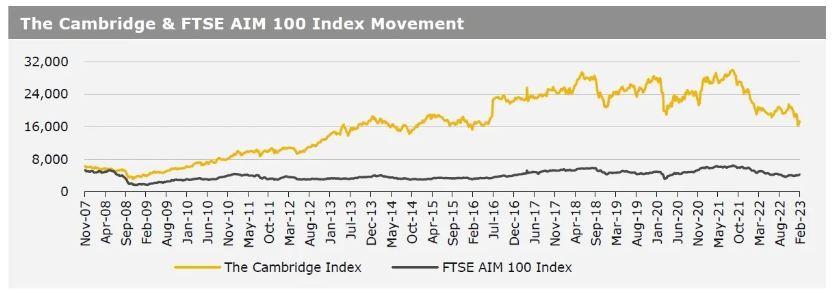

UK markets closed higher last week, after the Bank of England forecasted a ‘shallower’ recession in 2023. On the macro front, UK’s BRC shop price index climbed in December, registering its biggest annual increase since at least 2006, amid increase in fresh food costs. Further, UK manufacturing PMI advanced in January, while the nation’s services PMI fell less than expected in the same month. Meanwhile, UK’s consumer credit demand rose less than expected in December, while the nation’s mortgage approvals eased to a 31-month low in December, amid higher interest rates. Additionally, UK’s Nationwide housing prices fell for a fifth straight month in January, on inflationary pressures and rise in borrowing costs. The FTSE 100 index advanced 1.8% to settle at 7,901.8, while the FTSE AIM 100 index rose 3.3% to close at 4,308.0 Meanwhile, the FTSE techMARK 100 index gained 3.7% to end at 6,661.6.

US markets ended mixed in the previous week. On the data front, the US Dallas Fed manufacturing business index improved in January, while the Chicago Purchasing Managers’ Index declined less than expected in January. Additionally, the US JOLTS job openings unexpectedly rose in December, indicating strong demand for labour, while the nation’s initial jobless claims unexpectedly declined to a 9-month low in the week ended 27 January 2023. Furthermore, the US nonfarm payrolls unexpectedly jumped in January, while the nation’s unemployment rate unexpectedly dropped to its lowest since 1969 in January. On the contrary, the ISM manufacturing PMI dropped more than expected in January, as higher interest rates dampened demand for goods, while the nation’s construction spending eased in December. Additionally, the US factory orders advanced less than anticipated in December. The DJIA index fell 0.2% to end at 33,926.0, while the NASDAQ index gained 3.3% to close at 12,007.0.