Bango, up 6.7%, announced that following the signing of a long-term Digital Vending Machine® contract in FY23 by a top 5 US operator, the service has now launched. This launch triggers the start of the associated license revenue which adds a minimum of $2m additional Annualized Recurring Revenue (ARR).

Nexteq, up 3.0%, in its audited full-year results for the 12 months ended 31 December 2023, announced that revenues dropped to $114.3m from $119.9m recorded in the previous year. Profit before tax widened to $12.9m from $8.8m. The company has proposed a dividend of 3.3p per share (2022: 3.0p per share), payable on 23 August 2024.

Quartix Technologies, up 2.9%, announced that it has introduced its new affordable dashcam solution into the growing market for video telematics, initially in the UK with plans to launch in the US later in 2024.

Sareum Holdings, down 38.6%, in its trading update, announced that it expects to report an operating loss of £2.5m (2022: £1.7m), reflecting the cost of continued and additional investment into clinical research conducted during the period for the furtherance of its SDC-1801 autoimmune disease programme. The company will release its results for the half-year to 31 December 2023 in the week beginning 25 March 2024.

1Spatial, down 4.8%, in its trading statement for the financial year ended 31 January 2024, announced that it expects total revenue to be no less than £32.1m with approximately 55% (FY2023: 50%) represented by recurring revenue. Additionally, its adjusted EBITDA was expected to be no less than £5.5m (FY2023: £5.0m) and reported profit before tax not less than £1.0m (FY2023: £1.0m), reflecting increased finance costs due to the high-interest rate environment. As at 31 January 2024, the Group's net cash stood at £1.1m (£3.1m as at 31 January 2023). Further, the company expects to release its audited final results for the year ended 31 January 2024 on 24 April 2024.

IQGeo Group, down 0.8%, announced that it will release its results for the 12 months ended 31 December 2023 on 20 March 2024.

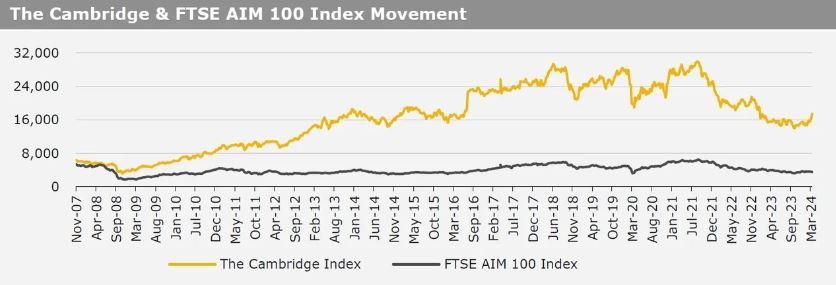

UK markets ended mostly lower last week. On the data front, UK’s manufacturing production remained flat as expected in January, while the nation’s industrial production unexpectedly dropped in January. Moreover, UK’s ILO unemployment rate unexpectedly rose in the three months to January. Meanwhile, UK’s gross domestic product grew as expected in January, driven by growth in services and construction output. Additionally, UK’s RICS housing price balance index rose more than expected in February. The FTSE techMARK 100 index lost 1.2% to end at 6,885.9, while the FTSE AIM 100 index fell 0.5% to close at 3,561.1. Meanwhile, the FTSE 100 index advanced 0.9% to settle at 7,727.4.

US markets ended lower in the previous week, following more-than-expected US inflation data raised uncertainty over the timings of rate cuts by the US Federal Reserve. On the macro front, the US retail sales advanced less than expected in February, indicating a slowdown in consumer spending, while the nation’s Michigan consumer sentiment index unexpectedly fell in March. Moreover, the US NY Empire State manufacturing index declined sharply in March. Meanwhile, the US consumer price index rose more than expected in February, while the nation’s producer price index climbed more than anticipated in February, on higher gasoline prices. Additionally, the US weekly jobless claims unexpectedly dropped in the week ended 08 March 2024. The DJIA index marginally fell to end at 38,714.8, while the NASDAQ index lost 0.7% to close at 15,973.2.