Johnson Matthey, up 16.0%, announced that investment arm of New York-based industrial firm, Standard Industries has raised its stake to over 10.0% in the chemicals company.

Kier Group, down 1.1%, announced the promotion of James Martin to health, safety, wellbeing & sustainability Director and head of the Group's Responsible Business team.

Aferian, up 4.2%, in its unaudited results for the six months ended 31 May 2023, announced that revenues fell to $23.35m from $44.52m recorded in the same period previous year. Loss before tax widened to $8.65m from $0.81m. The Board has not proposed an interim dividend (H1 2022: 1.0p/1.26 US cents). Separately, the company announced that it has appointed Allen Broome as a Non-Executive Director, with immediate effect.

GRC International Group, up 2.0%, announced that it has introduced an all-encompassing suite of products specifically designed to empower businesses in achieving compliance with the new Digital Operational Resilience Act (DORA). This comprehensive suite includes an array of resources, tools, training, and consultancy services to assist organisations in navigating the complex landscape of digital operational resilience.

Tristel, up 1.5%, today, announced the submission of its application to Health Canada to approve Tristel ULT as a Class II Medical Device for endocavity ultrasound probes and skin surface transducers.

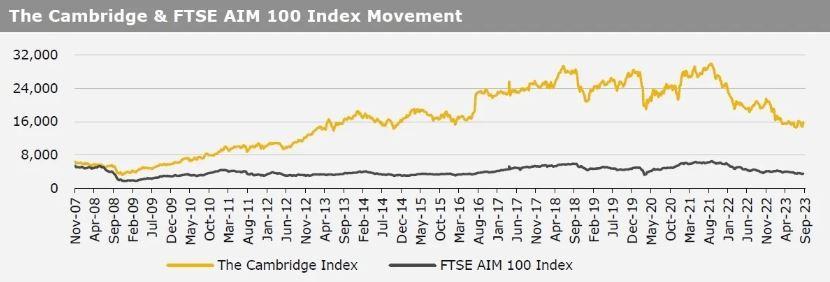

Cambridge Cognition, unchanged at 92.0p, today, announced that it would release its unaudited interim results for the six months ended 30 June 2023 on 26 September 2023.

Sareum Holdings, down 1.3%, today, announced that it has successfully dosed the first subjects in the multiple ascending dose part of its Phase 1a clinical trial for lead programme SDC-1801. This follows approval by the safety review committee granted upon review of preliminary data generated from the initial three cohorts in the single ascending dose part of the study.

Kier Group, down 1.1%, announced the promotion of James Martin to health, safety, wellbeing & sustainability Director and head of the Group's Responsible Business team.

UK markets ended higher last week, on China’s stimulus measures. On the macro front, UK manufacturing PMI to a 39-month low in August, amid weaker domestic and export conditions. Additionally, the Nationwide house price index dropped at its fastest pace since 2009 in August, due to increase in mortgage costs, while the nation’s BRC shop price index rose at its slowest pace since October 2022 in July. The FTSE 100 index advanced 1.7% to settle at 7,464.5, while the FTSE AIM 100 index rose 1.4% to close at 3,535.4. Also, the FTSE techMARK 100 index gained 2.0% to end at 6,363.7.

US markets ended higher in the previous week, amid expectations for a pause in rate hike by the US Federal Reserve. On the data front, the US nonfarm payrolls rose by more than anticipated in August, while the nation’s weekly jobless claims unexpectedly fell to its lowest level in four weeks in the week ended 25 August 2023. Additionally, the ISM manufacturing PMI rebounded in August, while the Chicago Purchasing Managers' Index climbed in July. Moreover, the US pending home sales advanced for a second straight month in July. Meanwhile, the US economy grew less than expected in 2Q23, while the nation’s consumer confidence index fell more than expected in August, amid renewed worries over inflation. Moreover, the US unemployment rate unexpectedly advanced in August, while the nation’s JOLTs job openings fell to its lowest level since March 2021 in July. Additionally, the US ADP employment climbed by less than anticipated in August. The DJIA index rose 1.4% to end at 34,837.7, while the NASDAQ index gained 3.2% to close at 14,031.8.