DS Smith, down 0.7%, has partnered with E.ON to develop a new Waste To Energy (WTE) and Combined Heat and Power plant at the Aschaffenburg paper mill in Germany.

Kier Group, up 6.6%, announced in its trading update for the six months ended 31 December 2022, that its half yearly results are anticipated to be in line with the Board's expectations. The order book as of 31 December 2022 is expected to be around £10.1b, an increase of approximately 3% from the year-end position (FY22: £9.8b). Net debt as at 31 December 2022 is anticipated to be similar to 31 December 2021. Further, the company will publish its results for the six months ended 31 December 2022 on 9 March 2023.

Frontier Developments, up 9.1%, in its interim results for the six months to 30 November 2022, announced that revenues jumped 16.0% to £57.1m from £49.1m recorded in the same period a year ago. Profit before tax stood at £6.7m compared to a loss of £1.7m. Cash balance stood at £42.6m as at 30 November 2022.

Cambridge Cognition Holdings, up 1.3%, announced that it has acquired Canada-based Winterlight Labs in a cash and stock deal worth £7m.

Quixant, up 0.3%, announced in its trading update for the financial year ended 31 December 2022, that it expects to report full year revenues of $119.9m, up 38% year-on-year. Further, the Group expects adjusted profit before tax to be slightly ahead of market expectations. Net cash as at 31 December 2022 increased to $12.9m from $12.0m as at 30 June 2022 Additionally, the company announced that it expects to release its annual results for 2022 on 21 March 2023.

CyanConnode Holdings, down 2.9%, announced that it has appointed Zeus Capital Limited as a Joint Broker, with immediate effect.

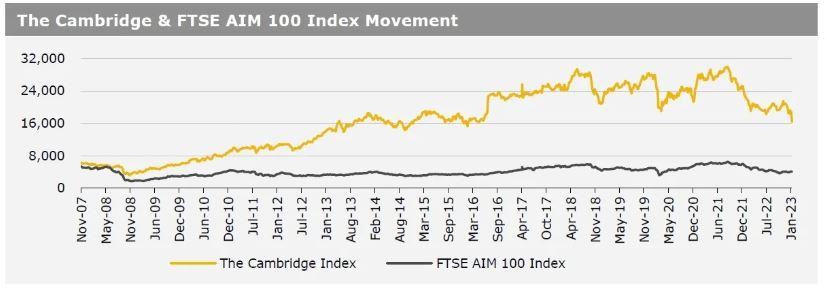

UK markets closed lower last week, amid rising concerns over recession and rate hikes by major central banks. On the macro front, UK’s inflation eased for a second straight month in December, due to the slowdown in motor fuel inflation, while the nation’s retail sales unexpectedly fell in December, as shoppers cut back on spending. Further, UK’s GfK consumer confidence unexpectedly dropped to near 50-year low in January, amid concerns over cost-of-living crisis and economic slowdown. Additionally, UK’s DCLG house price index climbed less than anticipated in November, while the RICS house price balance fell to a 13-year low in December. Meanwhile, UK’s unemployment rate remained steady as expected in November. The FTSE 100 index declined 0.9% to settle at 7,770.6, while the FTSE AIM 100 index fell 1.4% to close at 4,090.6. Meanwhile, the FTSE techMARK 100 index lost 1.3% to end at 6,442.8.

US markets ended lower in the previous week, following disappointing US economic data and hawkish remarks from Federal Reserve (Fed) officials. On the data front, the US producer price index (PPI) declined in December, as the costs of energy products and food declined, while the nation’s retail sales fell by the most in a year in December, amid declines motor vehicles purchases and a range of other goods. Moreover, the US NY Empire State manufacturing index declined in January, while the nation’s industrial production recorded its biggest monthly decline since September 2021 in December. Further, the US building permits dropped in December, while the nation’s housing starts declined for a fourth straight month in the same month. Also, the US existing home sales fell to a 12-year low in December, amid higher mortgage rates. Meanwhile, the US initial jobless claims unexpectedly declined to its lowest level since September 2022 in the week ended 13 January 2023. The DJIA index fell 2.7% to end at 33,375.5, while the NASDAQ index gained 0.6% to close at 11,140.4.