Johnson Matthey, down 3.2%, announced that its jointly developed Fischer Tropsch CANS technology with BP has been chosen by Strategic Biofuels for their project which aims to produce the lowest carbon footprint liquid fuel.

Darktrace, down 1.9%, announced the general availability of Darktrace Newsroom TM, an AI-driven system that continuously monitors open-source intelligence sources for new critical vulnerabilities and assesses each organization's exposure through its in-depth knowledge of their unique external attack surface. Separately, the company announced that it has appointed Ernst & Young LLP to provide an additional independent third-party review of its financial processes and controls. Additionally, the company intends to release its interim results for the six months ended 31 December 2022 on 8 March 2023.

Tristel, up 9.5%, in its interim results for the six months to 31 December 2022, announced that revenues rose 16.0% to £17.5m from £15.1m recorded in the same period a year ago. Profit before tax stood at £2.4m, compared to a loss of £1.2m. The company has maintained its interim dividend at 2.62p per share.

Quartix Technologies, up 6.9%, today, in its full year audited results for the year ended 31 December 2022, announced that group revenues rose 7.9% to £27.5m from £25.5m recorded in the previous year. Profit before tax widened to £5.5m from £5.4m. The board has proposed a final dividend of 6.30p per share (2021: 7.00p) including 3.85p for supplementary dividend (2021: 5.10p) giving a total dividend for the year of 7.80p per share.

GetBusy, up 6.2%, announced the appointment of finnCap as Nominated Adviser and sole Broker to the Company, with immediate effect.

Bango, up 2.1%, announced that it has partnered with Dropbox, a leading cloud storage service that allows one to backup and sync files across multiple devices.

Oracle Power, down 3.9%, announced that it has joined the Dii Desert Energy as an Associate Partner.

Quixant, down 3.0%, announced that it expects to publish its results for the year ended 31 December 2022 on 21 March 2023.

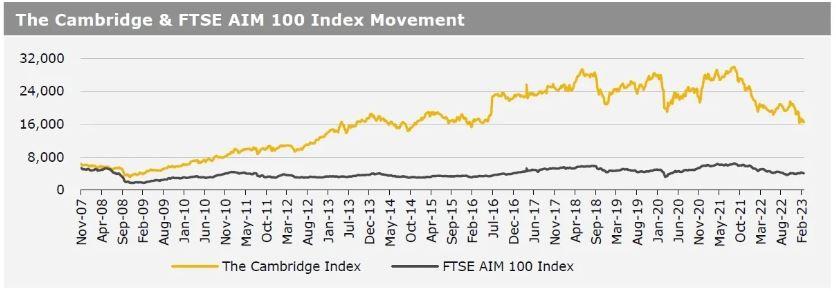

UK markets closed mostly lower last week, following dismal corporate earnings reports and concerns over further interest rate hikes. On the macro front, UK’s manufacturing PMI advanced to a 7-month high in February, while the nation’s services PMI unexpectedly climbed to an 8-month high in the same month. Additionally, UK’s GfK consumer confidence climbed to a 10-month high in February, while the nation’s public sector net borrowing recorded a surplus in January. The FTSE 100 index declined 1.6% to settle at 7,878.7, while the FTSE AIM 100 index fell 1.8% to close at 4,069.4. Meanwhile, the FTSE techMARK 100 index gained 0.4% to end at 6,688.5.

US markets ended lower in the previous week, amid renewed concerns over aggressive rate hikes by the US Federal Reserve (Fed). On the data front, the US gross domestic product (GDP) grew less than anticipated in 4Q22, while the nation’s existing home sales unexpectedly dropped for a twelfth consecutive month in January. Meanwhile, both, the US manufacturing and services PMIs increased more than estimated in February, while the nation’s Chicago Fed National Activity Index rebounded in January. Moreover, the US initial jobless claims unexpectedly fell in the week ended 17 February 2023, while the nation’s Michigan consumer sentiment index advanced to a 13-month high in February. The DJIA index fell 3.0% to end at 32,816.9, while the NASDAQ index lost 3.3% to close at 11,394.9.