AVEVA Group, down 0.2%, announced that the Court Meeting and General Meeting in light of the Increased Offer by which the entire issued and to be issued share capital of AVEVA will be acquired by Bidco has been adjourned. The Court Meeting would now start at 11.30 a.m. and the General Meeting would start at 11.45 a.m. (or as soon thereafter as the Court Meeting concludes or is adjourned) on 25 November 2022.

DS Smith, down 3.5%, announced that it has appointed Richard Pike as Group Finance Director and Executive Director, with effect from Adrian Marsh's retirement next summer.

Darktrace, down 7.3%, announced that it is witnessing strong demand for its new Darktrace PREVENT ™ product family as organisations seek to prevent cyber-attacks, rather than waiting for breaches to happen.

Xaar, up 1.2%, announced that it has launched its new printhead the Xaar Aquinox to improve print quality, nozzle open time and energy efficient operation for aqueous inkjet printing.

Oracle Power, down 10.5%, announced that its subsidiary, Oracle Energy, has signed a letter of Intent (LOI) with TÜV SÜD to explore green hydrogen and green ammonia certification relating to the green hydrogen project in development in Pakistan. Separately, the company announced that it has appointed Buchanan as its retained Public Relations and Financial Communications Adviser, with immediate effect.

Sareum Holdings, down 4.4%, today, announced the publication of data from a Phase I/2 trial of SRA737, a clinical-stage oral, selective small molecule Checkpoint kinase 1 (Chk1) inhibitor, in combination with commonly used chemotherapeutic agent gemcitabine, in the 15 November edition of Clinical Cancer Research. The company retains a 27.5% economic interest in SRA737 arising from its collaboration in the discovery and early development of the molecule.

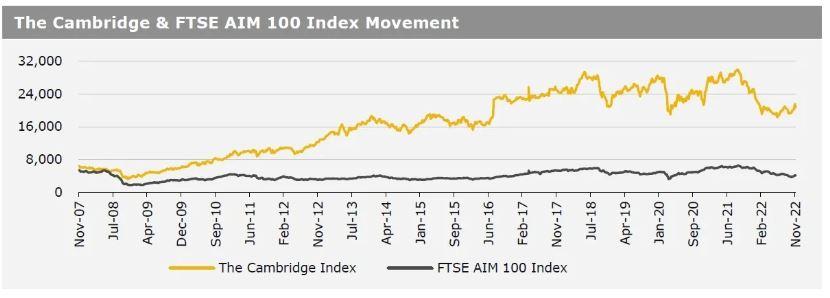

UK markets closed mostly higher last week, following optimistic comments from the European Central Bank members. On the macro front, UK’s inflation climbed to a 41-year high level in October, amid soaring energy and food prices, while the nation’s retail sales rebounded in October. Also, UK’s GfK consumer confidence index advanced for a second consecutive month in November, as concerns over political instability eased. Meanwhile, UK’s ILO unemployment rate rose more than anticipated in September. In major news, Britain’s Finance Minister Jeremy Hunt announced tax rises and spending cuts in an effort to tame inflation. The FTSE 100 index advanced 0.9% to settle at 7,385.5, while the FTSE techMARK 100 index gained 0.7% to end at 6,275.8. Meanwhile, the FTSE AIM 100 index fell 2.8% to close at 4,043.6.

US markets ended lower in the previous week, amid worries about hawkish statements from US Federal Reserve officials. On the data front, the US producer price inflation fell to a 14-month low in October, further confirming that inflation may be easing, while the nation’s industrial production unexpectedly dropped in the same month. Moreover, both, the US building permits and housing starts dropped in October, amid rising mortgage rates. Also, the NAHB housing market index fell for an 11th straight month in October, while the nation’s existing home sales dropped for ninth straight month in October. Meanwhile, the US retail sales climbed to an 8-month high level in October, driven by higher gas prices and auto sales, while the nation’s initial jobless claims declined more than expected in the week ended 11 November 2022, despite surge in technology layoffs. The DJIA index marginally fell to end at 33,745.7, while the NASDAQ index lost 1.6% to close at 11,146.1.