Johnson Matthey, up 1.6%, in its pre-close trading update, announced that it expects strong performance in underlying operating profit for the first half of the year, (excluding Catalyst Technologies and Value Businesses), driven by ongoing efficiency improvements and strong trading in the PGM Services business.

Science Group, down 0.5%, today, in its trading update, announced that it is maintaining strong momentum despite market volatility. The company achieved record adjusted operating profit in H1 and realised a £24m exceptional pre-tax gain from a strategic investment.

1Spatial, up 13.5%, today, in its interim results, announced that revenues advanced to £17.65m from £16.25m recorded in the same period of the previous month. Loss before tax widened to £0.31m from £0.16m.

Quartix Technologies, up 3.5%, in its trading update, announced that strong performance for the nine months to 30 September 2025, with Q3 results exceeding expectations.

Dialight, up 1.2%, in its trading update, reported softer market demand and slightly lower sales due to tariff uncertainty and a weak economic environment.

SDI Group, up 0.2%, announced that it has appointed Stifel Nicolaus Europe Limited as its joint corporate broker, with immediate effect.

Sareum, down 39.2%, announced that it has discontinued its 16-week GLP preclinical toxicology study for SDC-1801 following safety findings observed by the third-party provider of the study. The issues disproportionately affected the control group, which received an inactive dosing solution, suggesting the findings are unlikely to be related to SDC-1801. Dosing has been terminated, and the study will be formally closed after scheduled analyses.

Oracle Power, down 33.3%, announced the booking of a grade control drill rig from Australian Surface Drilling for its Northern Zone Gold Project. The drilling programme, set to commence in three weeks, aims to expand the mineralised footprint of the project.

Netcall, down 3.3%, in its final results, announced that its revenue advanced to £47.96m from £39.06m recorded in the previous year. Profit before tax narrowed to £5.07m from £6.33m. The board has proposed a final dividend of 0.94p per share. If approved at the company's 2025 annual general meeting, the final dividend will be paid on 9 February 2026 to shareholders.

Tristel, down 1.2%, today, in its final results, announced that its revenue advanced to £46.46m from £41.93m recorded in the previous year. Profit before tax widened to £8.42m from £7.08m. Its cash and cash equivalents stood at £8.64m for the year ended 30 June 2025. The board has declared a dividend of £8.52p for the year.

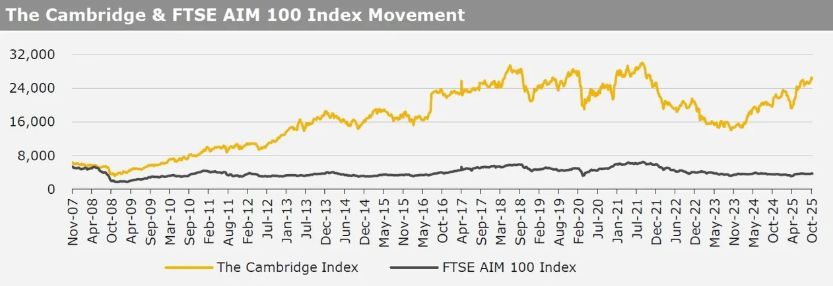

UK markets ended lower last week, amid mounting trade tensions between the US and China. On the data front, the UK Halifax house prices unexpectedly declined in September. Meanwhile, the UK RICS housing price balance index rose more than expected in September. The FTSE 100 index declined 0.7% to settle at 9,427.5, while the FTSE AIM 100 index fell 1.4% to close at 3,746.1. Meanwhile, the FTSE techMARK 100 index lost 1.1% to end at 8,084.0.

US markets ended lower in the previous week, after US President Donald Trump threatened new trade tariffs on China. On the macro front, the US Michigan consumer sentiment index fell less than expected in October. Separately, US FOMC minutes reported that most officials expect further interest rate cuts this year, though many remain cautious due to persistent inflation risks. The DJIA index fell 2.7% to end at 45,479.6, while the NASDAQ index lost 2.5% to close at 22,204.4.