Johnson Matthey, up 2.1%, announced that it has signed a five-year supply contract with Sarepta Therapeutics Inc, to continue supplying regulatory starting materials to support Sarepta's phosphorodiamidate morpholino oligomer and peptide phosphorodiamidate morpholino oligomer programmes used for the treatment of Duchenne Muscular Dystrophy.

Xaar, up 17.2%, announced that it will release its interim results for the six months ended 30 June 2020 on 30th September 2020.

Cambridge Cognition, up 3.8%, announced that it has bagged a £2m contract as the cognitive assessment partner for three late phase clinical trials for a pharmaceutical company's lead drug candidate for patients with schizophrenia.

Kier Group, up 0.3%, announced today that it has appointed Alison Atkinson to its Board of Directors, effective from 15 December 2020.

CyanConnode, down 5.4%, in its audited results for the 15-month period ended 31 March 2020, stated that revenue declined to £2.45m from £4.47m recorded in the same period of the previous year. Further, its basic and diluted loss per share stood at 3.27p, compared to 4.60p. Separately, the company announced that it has secured a new order for the Indian state-owned utility, Madhya Pradesh Paschim Kshetra Vidyut Vitaran Company Ltd (MPWZ), for 350,000 Omnimesh Modules.

IQGeo Group, down 2.1%, announced that it has secured a new contract for software licences and services with a large tier 1 telecoms network operator. The contract has an overall value of £0.6m and comprises both a software licence subscription to be recognised over the next three years and certain implementation services to be recognised over the next two years. Separately, today the company announced that Richard Petti and Haywood Chapman would conduct a live presentation regarding interim results for the 6 months ended 30th June 2020 via the Investor Meet company platform on 14th September.

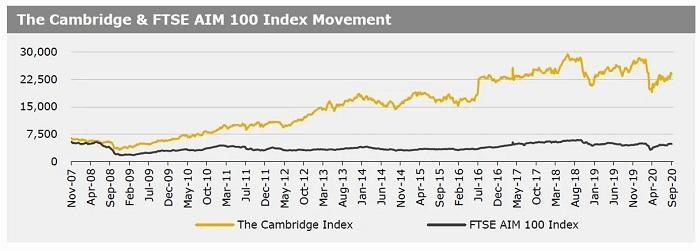

UK markets closed lower last week, as investors mulled over the latest reading on the UK’s services sector. British services PMI registered its strongest level since April 2015 in August, as businesses and consumers kick started spending after the loosening of coronavirus-led lockdowns. However, job losses accelerated in August despite an upturn in demand. British factory output rose in August at its fastest pace in more than six years. Further, UK house prices reached a new all-time high in August. In contrast, British construction PMI suffered a surprise slowdown in August. The FTSE 100 index declined 2.8% to settle at 5799.1, while the FTSE AIM 100 index fell 2.1% to close at 4790.9. Also, the FTSE techMARK 100 index lost 2.8% to end at 5605.7.

US markets ended lower in the previous week, after the US nonfarm payrolls came in less than expected for August, reflective of a slowdown in the economic recovery. Meanwhile, private sector employment increased less-than-expected in August. The ISM manufacturing PMI expanded more than anticipated in August, as the industry's recovery from coronavirus shutdowns picked up. Further, construction spending rose in July. The Federal Reserve’s Beige Book report showed that the US economy expanded modestly in August, but with many parts of the country experiencing slower growth during the pandemic, as some companies made temporary layoffs permanent. The DJIA index fell 1.8% to end at 28133.3, while the NASDAQ index lost 3.3% to close at 11313.1.