DS Smith, down 2.4%, announced that it has ordered a supply of advanced consistency measurements from Valmet for its paper facility in Lucca, Italy. The delivery includes seven Valmet Microwave Consistency Measurements (Valmet MCA), six Valmet Blade Consistency Measurements, and six Valmet Optical Consistency Measurements (Valmet OCR and OC2R).

Feedback, up 17.2%, in its audited results for the six months to 30 November 2023, announced that revenues dropped to £0.4m from £0.6m recorded in the same period of the previous year. Loss before tax widened to £2.1m from £1.6m. Its cash balance stood at £5.4m as at 30 November 2023. Separately, the company announced that it has signed a deal with the radiology specialist, Medical Imaging Partnership (MIP) to pilot its Bleepa-CareLocker for delivery in multiple clinical pathways to its customers in the UK private healthcare sector.

1Spatial, up 12.6%, announced that it has secured a 12-month contract with UK Power Networks, for its Traffic Management Plan Automation (TMPA) solution, under the 1Streetworks brand in the UK (1Streetworks). The contract will deliver a minimum of £0.34m of SaaS revenue.

Oracle Power, down 33.3%, announced that it has launched an Environmental & Social Impact Assessment (ESIA) for the Renewable Power plant on its project land site in Jhimpir, in the Sindh Province of Pakistan.

Xaar, down 14.3%, announced that it has appointed Stuart Widdowson as a Non-Executive Director to the Board, with effect from 27 February 2024.

Cambridge Cognition Holdings, down 4.9%, announced that it has entered into a new strategic partnership with ActiGrap to enhance the adoption of digital measurements for central nervous system (CNS) trials.

Quartix Technologies, down 3.5%, announced that it has appointed Ian Spence as independent Non-Executive Director, with effect from 19 February 2024.

Dialight, down 0.6%, in its interim results, announced that revenues fell to £75.6m from £88.9m recorded in the same period of the previous year. Loss before tax widened to £10.2m from £1.1m. The Board is not declaring an interim dividend payment for 2023 (2022: nil).

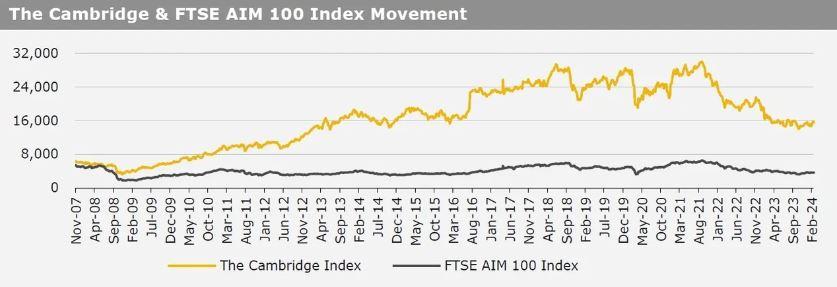

UK markets closed mostly lower last week, as British consumer sentiment fell in February. On the macro front, UK’s manufacturing PMI advanced less than expected in February, while the nation’s GfK consumer confidence dropped for the first time in four months in February. Additionally, UK’s public sector net borrowing surplus widened less than anticipated in January. On the flipside, UK’s services PMI climbed more than expected in February, while the nation’s Rightmove house price index rose in February. The FTSE 100 index declined 0.1% to settle at 7,706.3, while the FTSE AIM 100 index fell 1.7% to close at 3,629.6. Meanwhile, the FTSE techMARK 100 index gained 0.7% to end at 6,915.5.

US markets ended higher in the previous week, following upbeat US quarterly corporate earnings. On the data front, the US manufacturing PMI rose at its fastest pace since September 2022 in February, while the nation’s existing home sales advanced in January, amid lower mortgage interest rates. Moreover, the US weekly jobless claims unexpectedly declined in the week ended 16 February 2024. Meanwhile, the US services sector dropped more than anticipated in February, while the nation’s Chicago Fed National Activity Index fell in January. Separately, the US FOMC minutes indicated that policymakers were concerned about the risks of cutting interest rates too soon, with the uncertainty associated with how long a restrictive monetary policy stance would need to be maintained to return inflation to the US central bank's 2% target. The DJIA index rose 1.3% to end at 39,131.5, while the NASDAQ index gained 1.4% to close at 15,996.8.