Frontier Developments, down 0.7%, announced that David Gammon has stepped down from the Board after serving a full term as Chairman and would be replaced by David Wilton, who joined the Board on 22 September 2022. These changes would be effective 1 December 2022.

Bango, down 2.8%, announced that McAfee has launched its e-distribution operations in Europe through the Bango Platform, collaborating initially with Onestream. The Bango Platform allows retailers to standardise e-distribution and remove the complexity of online distribution channels to promote their products through online distribution channels.

CyanConnode Holdings, down 3.8%, announced in its trading update for the six-month period ended 30 September 2022, that trading was in line with market expectations and that revenue for the 12-month ended 31 March 2023, is also forecasted to be in line with market expectations. Also, the company announced that it would release its interim results for the six-month period ended 30 September 2022, on 14 December 2022.

Oracle Power, down 2.1% to 0.2p, announced the purchase by Oracle Energy of State land through a long lease for 30 years with the Government of Sindh, for a land package of 7,000 acres located in Sindh, south-east Pakistan, where its flagship Green Hydrogen Project would be located.

GRC International Group, unchanged at 24.0p, announced that its IT Governance division has earned accreditation of CPD (Continued Professional Development) for a number of its instructor-led and self-paced training courses. This will allow the company to promote its training courses to a larger and wider pool of institutions.

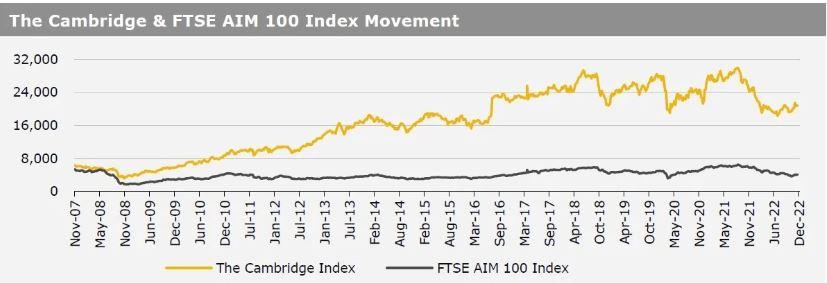

UK markets closed higher last week, amid optimism over slower interest rate hikes by the US Federal Reserve (Fed). On the macro front, UK’s BRC shop price index climbed in October, while the nation’s manufacturing PMI advanced more than expected in November. Meanwhile, UK’s consumer credit rose less than anticipated in October, while the nation’s mortgage approvals declined in the same month, as rising interest rates reduced demand for property. Moreover, UK’s Nationwide housing prices fell to its lowest level since June 2020 in November, amid rise in borrowing costs. The FTSE 100 index advanced 1.4% to settle at 7,556.2, while the FTSE AIM 100 index rose 1.2% to close at 4,129.4. Meanwhile, the FTSE techMARK 100 index gained 2.3% to end at 6,366.9.

US markets ended higher in the previous week, after US Fed Chairman, Jerome Powell announced that the central bank could slow the pace of interest rate hikes as soon as December. On the data front, the US annualised gross domestic product (GDP) grew faster than anticipated in 3Q 2022, while the nation’s personal income climbed more than expected in October, while the nation’s personal spending jumped in the same month, as inflation cooled. Additionally, US nonfarm payrolls advanced by more than estimated in November, initial jobless claims declined more than anticipated in the week ended 25 November 2022. Meanwhile, the US ISM manufacturing PMI registered its first decline in 29 months in November, while the nation’s consumer confidence index declined to a four-month low in November amid concerns over high inflation and rising borrowing costs. Further, pending home sales fell for fifth straight month in October. The DJIA index rose 1.8% to end at 34,429.9, while the NASDAQ index gained 0.7% to close at 11,461.5.