AVEVA Group, up 0.9%, in its interim results for the six months ended 30 September 2022, announced that revenues advanced 7.3% to £553.80m from £516.10m recorded in the same period a year ago. The board has declared an interim dividend of 13.0p per share (H1 FY22: 13.0p).

Abcam, up 11.7%, along with NanoString Technologies announced that they have expanded their long-standing relationship with a new agreement to co-market Abcam antibodies for NanoString’s high-plex spatial multiomic solutions.

Darktrace, down 13.5%, today, announced that it is witnessing strong demand for its new Darktrace PREVENT™ product family.

SDI, up 0.3%, announced that Mike Creedon and Ami Sharma will provide a live presentation relating to the Group's Interim Results for the six months to 31 October 2022 on 7 December 2022 at 4:00pm GMT.

Netcall, up 0.6%, announced that Non-Executive Director, Michael Neville intends to step down from his position. Additionally, the company announced that its annual general meeting (AGM) will be held at 10.30 am on 8 December 2022.

GRC International Group, unchanged at 24.0p, today, announced that its IT Governance business has inked a three-year contract with a South Asian financial institution to assist the organisation with its SWIFT compliance.

Oracle Power, unchanged at 0.3p, announced that its Chief Executive Officer Naheed Memon would be hosting an investor webinar on 17 November at 17:00. Today, the company announced that its subsidiary, Oracle Energy, has signed a letter of Intent (LOI) with TÜV SÜD to explore green hydrogen and green ammonia certification.

Sareum Holdings, down 34.5%, announced that it has been notified by the UK Medicines and Healthcare Products Regulatory Agency that the Clinical Trial Authorization to assess the safety and tolerability of its principal programme SDC-1801 has not been approved.

Hilton Food Group, down 6.7%, in its trading update, announced that volume and revenue have been in line with the Board's expectations, with continued revenue growth compared to the same period last year.

Science Group, down 3.7%, announced that it has signed an agreement to acquire the entire issued and to be issued ordinary share capital of TP Group for a consideration of £17.53m.

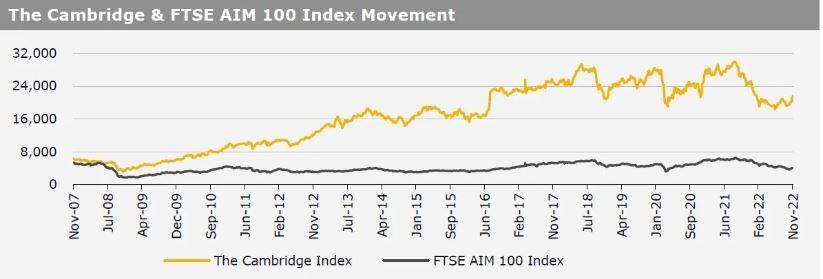

UK markets closed mostly higher last week, amid optimism over US consumer prices. On the macro front, UK’s industrial production rebounded in September, while the nation’s manufacturing output improved in September. Also, the nation’s trade deficit unexpectedly narrowed in September. Further, UK’s GDP dropped for the first time in six quarters in 3Q 2022, indicating the start of a long recession. Additionally, UK’s Halifax house prices unexpectedly fell at its fastest pace since February 2021 in October, amid rising interest rates, while the nation’s RICS housing price balance unexpectedly dropped for the first time in 28 months in October. The FTSE 100 index declined 0.2% to settle at 7,318.0, while the FTSE AIM 100 index rose 6.2% to close at 4,162.1. Meanwhile, the FTSE techMARK 100 index gained 2.6% to end at 6,233.8.

US markets ended stronger in the previous week, as a softer inflation data raised hopes that the Fed would slow the pace of rate hikes. On the data front, the US consumer price inflation fell to a 9-month low in October. Further, the US NFIB business optimism index declined to a three-month low in October, while the nation’s MBA mortgage applications fell to a 25-year low in the week ended 4 November 2022, amid rising borrowing costs. Additionally, the US initial jobless claims advanced more than anticipated in the week ended 4 November 2022. The DJIA index rose 4.1% to end at 33,747.9, while the NASDAQ index gained 8.1% to close at 11,323.3.