AVEVA Group, up 0.9%, announced that at the Court Meeting and the General Meeting held in connection with the acquisition of AVEVA by Bidco the requisite majority of eligible AVEVA Shareholders voted to approve the Scheme document and the requisite majority of eligible AVEVA Shareholders voted to pass the Special Resolution to implement the Scheme, including the amendment to AVEVA's articles of association, at the General Meeting.

Johnson Matthey, up 3.0%, announced in its interim results for the six months ended 30 September 2022, that revenues fell 14.0% to £7,328.0m from £8,503.0m recorded in the same period a year ago. Profit before tax stood at £188.0m compared to a loss of £4.0m.

Cambridge Cognition Holdings, up 2.1%, announced that it has signed a partnership deal with Luca Healthcare Limited to expand its footprint in the Chinese market.

Sareum Holdings, up 1.7%, announced the publication of data from a Phase I/2 trial of SRA737, a clinical-stage oral, selective small molecule Checkpoint kinase 1 (Chk1) inhibitor, in combination with commonly used chemotherapeutic agent gemcitabine, in the 15 November edition of Clinical Cancer Research.

Kier Group, up 0.3%, announced that its construction Managing Director, Liam Cummins would leave the firm at the end of the year.

GRC International Group, unchanged at 24.0p, today, announced that its IT Governance division has earned accreditation of CPD (Continued Professional Development) for a number of its instructor-led and self-paced training courses.

Oracle Power, down 7.8%, today, announced the purchase by Oracle Energy of State land through a long lease for 30 years with the Government of Sindh for a land package of 7,000 acres located in Sindh, south-east Pakistan, where its flagship Green Hydrogen Project will be located.

Dialight, down 4.7%, announced in its trading update for the 10-month period ended 30 October 2022, that its positive trading momentum has continued into the second half, with group revenue up 35% (CCY 23%) compared to the prior year. The company would publish its full year results for the year ending 31 December 2022 on 27 March 2023.

LPA Group, down 2.0%, announced in its trading update for the year ended 30 September 2022, that it reported improved trading performance compared to the second half of the prior year. Its orderbook remained high at £28m.

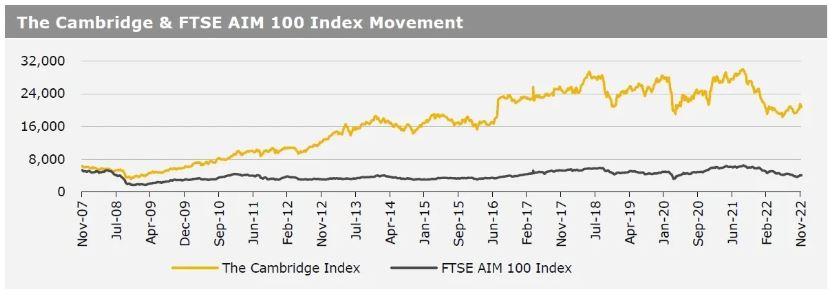

UK markets closed firmer last week on hopes of smaller rate hikes from the US Fed and as political tensions eased. On the data front, UK’s, both, manufacturing PMI and services PMI remained unchanged in November. Meanwhile, UK’s public sector net borrowing deficit narrowed more than expected in October. Separately, two Bank of England policy makers said the central bank must continue raising interest rates to bring inflation back to 2%. The FTSE 100 index advanced 1.4% to settle at 7,486.7, while the FTSE AIM 100 index rose 1.2% to close at 4,093.2. Meanwhile, the FTSE techMARK 100 index gained 2.3% to end at 6,418.7.

US markets ended higher in the previous week, as FOMC minutes signalled smaller interest rate hikes ahead. On the data front, the US Richmond Fed manufacturing index rose in November, while the nation’s durable goods orders rose more than anticipated in October. Additionally, the US new home sales rebounded rose in October, despite higher mortgage rates. Meanwhile, the US Chicago Fed National Activity Index fell in October, while the nation’s manufacturing PMI declined to a 30-month low in November, amid drop in new orders and output. Further, the US initial jobless claims climbed to a three-month high in the week ended 18 November 2022, amid rising layoffs in the technology sector. The DJIA index rose 1.8% to end at 34,347.0, while the NASDAQ index gained 0.7% to close at 11,226.4.