Darktrace PLC, down 2.1%, announced the launch of Darktrace HEAL™, its AI-enabled product, to help businesses more effectively prepare for, rapidly remediate, and recover from cyber-attacks.

Aferian, up 70.0%, announced that it has successfully raised around $4.0m through the issue of new ordinary shares at a price of 12.0p per new share.

Gaming Realms, up 7.0%, in its pre-close trading update for the half year to 30 June 2023, announced that revenues for H1'23 are anticipated to be approximately £11.4m and adjusted EBITDA of around £4.6m, up 34% and 32% respectively, on a yearly basis, driven by the continued growth of the Group's licensing business. The company would publish its interim results during the week commencing 11 September 2023. Bango, up 3.9%, in its trading update, announced that it has delivered strong trading performance during the first half of FY23, with revenue up 88% to $20.3m (1H22 $10.8m), in line with management expectations. As at 30 June 2023, net cash balance stood at $13.4m (31 December 2022: $9.5m). The company would release its interim results in September.

Tristel, up 0.7%, in its trading update, announced that revenues increased by 16.0% to £36.0m (FY 2022: £31.1m), ahead of market expectations. As at 30 June 2023, cash balances stood at £9.5m (30 June 2022: £8.9m).

CyanConnode Holdings, down 4.4%, in its final results announced that revenues rose to £11.73m from £9.56m recorded in the previous year. Loss before tax widened to £3.45m from £1.18m. The Directors do not recommend the payment of a dividend (2022: £nil).

Quartix Technologies, unchanged at 235p, today, in its interim results, announced that revenues rose to £14.62m from £13.33m recorded in the same period previous year. Profit before tax narrowed to £2.42m from £2.59m. Oracle, unchanged at 0.1p, in its Q2 2023 update, announced that its trading performance in the second quarter has been extremely productive.

Science Group, unchanged at 415.0p, in its interim results, announced that revenues rose to £56.10m from £44.78m recorded in the same period previous year.

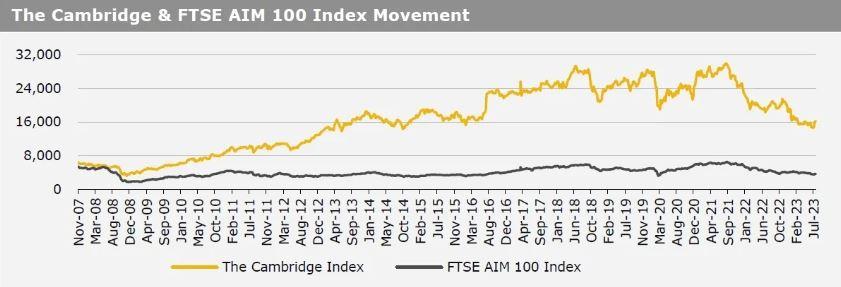

UK markets ended mostly lower last week. On the macro front, UK’s manufacturing activity sector fell to a 38-month low in July, amid drop in new orders while the nation’s services PMI dropped to a six-month low in July. The FTSE techMARK 100 index lost 1.8% to end at 6,583.5, while the FTSE AIM 100 index fell 0.2% to close at 3,648.9. Meanwhile, the FTSE 100 index advanced 0.4% to settle at 7,694.3

US markets ended higher in the previous week, following a series of upbeat corporate earnings reports and amid signs of easing inflation. On the macro front, the US economy accelerated in the second quarter of 2023, boosting chances of averting a recession, while the nation’s consumer confidence index advanced to a 2-year high in July, as inflation dropped. Additionally, durable goods orders rose in June, driven by rise in aircraft demand, while the US manufacturing PMI rebounded in July. Moreover, the US initial jobless claims unexpectedly fell to its lowest level since February in the week ended 21 July 2023. Further, the US pending home sales advanced for the first time since February in June, reflecting recovery in the housing market. Meanwhile, the US services sector fell more than anticipated in July, while the nation’s Chicago Fed National Activity index unexpectedly dropped in June. Separately, the US Federal Reserve raised its key interest rate by 25 basis points to 5.5%, reaching its highest level in more than 22 years, and signalled another rate hike in the coming months. The DJIA index rose 0.7% to end at 35,459.3, while the NASDAQ index gained 2.0% to close at 14,316.7.