Gaming Realms, up 3.8%, announced that it has launched a content in Connecticut, United States with its partner DraftKings. Initially, 5 games are available for play as part of the launch with 9 more to release soon.

Dialight, up 2.3% to 285.0p, announced that the company has appointed Nigel Lingwood as a Non-Executive Director, with effect from 1 November 2022. Oracle Power, up 2.3%, announced that its joint venture company, Oracle Energy Limited has signed a non-binding Memorandum of Understanding with Blue Carbon LLC to collaborate on a decarbonization roadmap to complement Oracle Energy's green hydrogen project in Pakistan.

Science Group, unchanged at 380.0p, today, announced that it has signed an agreement to acquire the entire issued and to be issued ordinary share capital of TP Group (not already owned by Science Group) for a consideration of £17.53m. Sareum Holdings, unchanged at 145.0p, in its audited results for the year ended 30 June 2022, announced that it reported nil revenues during the period. Loss before tax widened to £2.6m from £1.7m.

CyanConnode Holdings, unchanged at 13.3p, announced that the Conference of Power and Renewable Energy Ministers of State/ Union Territories was held on 14 and 15 October 2022 in Rajasthan, India which aimed on the financial sustainability and viability of the distribution industry, the modernization and improvement of the power infrastructure, and the creation of power systems that can supply power all over.

Aferian, down 32.7%, announced in its trading update, that revenues are forecasted to be 10% lower and would continue to remain lower until the first half of FY23.

SDI Group, down 6.7%, announced the acquisition of Fraser Anti-Static Techniques Limited for an expected total consideration of approximately £13.0 million.

Tristel, down 0.8%, announced, in its audited preliminary results for the year ended 30 June 2022, that revenues rose to £31.12m from £30.99m recorded in the same period a year ago. Profit before tax narrowed to £1.50m from £3.76m.

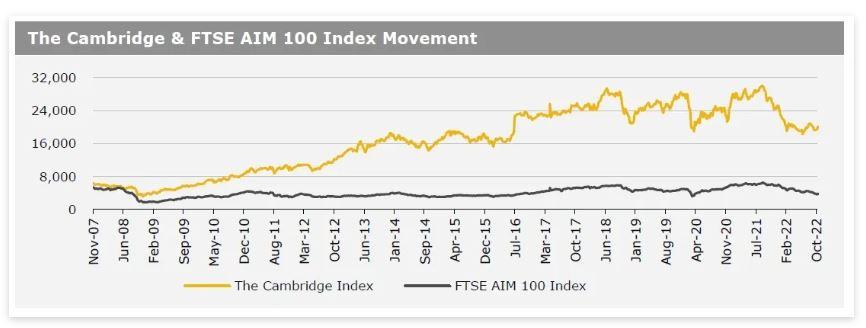

UK markets closed higher last week, after British politician Rishi Sunak was elected as UK’s new Prime Minister, thereby easing concerns over the ongoing political turmoil in the country. On the macro front, UK’s manufacturing PMI declined to a 29-month low in October, amid falling foreign demand while the nation’s services PMI dropped at its fastest pace since January 2021 in the same month. The FTSE 100 index advanced 1.1% to settle at 7,047.7, while the FTSE AIM 100 index rose 3.7% to close at 3,867.8. Meanwhile, the FTSE techMARK 100 index gained 3.1% to end at 6,022.7.

US markets ended firmer in the previous week, amid rising hopes for a less aggressive policy stance by the US Federal Reserve (Fed). On the data front, the US GDP rebounded in 3Q 2022, suggesting that a recession is unlikely while the nation’s durable goods orders climbed in September, driven by surge in aircraft orders. Additionally, the US Michigan consumer sentiment index advanced more than estimated in October. Meanwhile, the US manufacturing PMI dropped to a 28-month low in October, amid inflationary pressures, while the Richmond Fed manufacturing index declined more the expected in October. Further, the US goods trade deficit widened for the first time since March in September, as exports plunged, while the nation’s consumer confidence index declined to a three-month low in October, amid rising concerns about inflation and a possible recession. The DJIA index rose 5.7% to end at 32,861.8, while the NASDAQ index gained 2.2% to close at 11,102.5.