Johnson Matthey, up 0.8%, announced plans to sell its medical device components business in a bid to streamline its portfolio of assets.

Oracle Power, up 9.1%, announced that a joint Steering Committee has been established for the development of its 400 MW Green Hydrogen Project in Pakistan through its subsidiary Oracle Energy, a joint venture with HH Sheikh Ahmed Dalmook Al Maktoum. The planned Green Hydrogen Production facility, if fully commissioned, would produce an estimated 150,000kg of hydrogen per day (55,000 tons per annum), and would be one of the largest such projects in Asia. Separately, today, the company announced that it has signed a Memorandum of Understanding (MoU) between its subsidiary Oracle Energy and PetroChina International (Middle East) Company Limited (PCME) for cooperation and joint development of commercial avenues for Oracle Energy's planned Green Hydrogen Project in Sindh, Pakistan.

Tristel, up 6.6%, today announced that the USA Food and Drug Administration (FDA) has completed its review of its De Novo request for classification (Class II) of Tristel ULT as a high-level disinfectant and has granted its approval for immediate sale.

Frontier Developments, up 2.8%, announced that Charles Cotton would retire from his role as Non-Executive Director, with effect from 01 June 2023. Meanwhile, Leslie-Ann Reed has been appointed as an independent Non-Executive Director and Chair of the Audit Committee, effective 01 June 2023. Xaar, up 0.6%, announced that it has appointed Richard Amos as Non-Executive Director, with immediate effect.

Aferian, down 2.9%, in its trading update, announced that its trading performance was broadly in line with the board’s expectations. Further, demand for 24i's streaming video solutions demand remained robust. The board is confident in the long-term prospects for the group and expects to report growth in the first half of the current financial year. Separately, the company announced that it has secured further cash funding by way of a shareholder loan facility of up to £3.25m from its largest shareholder, Kestrel Partners LLP.

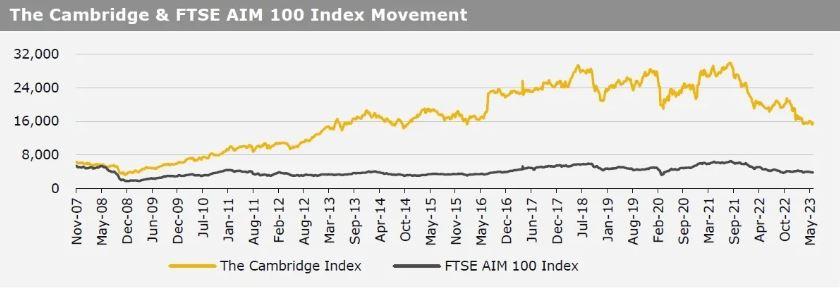

UK markets ended mostly lower last week. On the macro front, UK’s house prices fell at its fastest pace in nearly 14 years in May, amid higher mortgage rates, while the nation’s mortgage approvals unexpectedly fell in April, driven by higher interest rates. Additionally, Britain’s manufacturing PMI fell for a third consecutive month in May. Meanwhile, UK’s BRC shop price index rose to its highest level since 2005 in April. The FTSE 100 index declined 0.3% to settle at 7,607.3, while the FTSE AIM 100 index fell 0.1% to close at 3,772.9. Meanwhile, the FTSE techMARK 100 index gained 0.4% to end at 6,820.5.

US markets ended higher in the previous week, on robust US jobs reports and after the US Senate passed a bill to raise the debt ceiling limit. On the macro front, the US ADP employment climbed in May, while the nation’s job openings advanced in April. Moreover, the US non-farm payrolls rose by more-than-expected in May. On the other hand, the US ISM manufacturing PMI contracted for a seventh straight month in May, following a decline in new orders, while the Dallas Fed manufacturing index declined to a 3-year low in May. Additionally, the Chicago Purchasing Managers’ Index contracted for a ninth straight month in May, while the nation’s consumer confidence dropped to a six-month low in May, amid concerns over the outlook for business conditions. The DJIA index rose 2.0% to end at 33,762.8, while the NASDAQ index gained 2.0% to close at 13,240.8.