Johnson Matthey, up 0.2%, announced that its AGM would be held on 20 July 2023 at 11.00 am at Herbert Smith Freehills, Exchange House, Primrose Street, London EC2A 2EG.

Darktrace, up 21.3%, unveiled its new risk and compliance (AI) models, DETECT and RESPOND to protect its 8,400 worldwide customers from potential attacks conducted through the generative AI tools.

Frontier Developments, up 3.0%, in its trading update, announced that its trading performance has been in line with expectations. During FY23, the company delivered around £104m in revenue, supported by robust performance from the existing portfolio of games. As at 31 May 2023, the cash balance stood at £28m. Meanwhile, the company said it has completed its review of its Foundry games label for third-party publishing.

Cambridge Cognition, up 2.5%, announced that it has secured a £2 contract for a key cancer therapy trial, which will provide its proprietary cognitive assessments (CANTAB®) as an exploratory endpoint, with revenue expected over the next five years.

1Spatial, unchanged at 48.5p, today, announced that it has secured the first two contracts for its newly launched Traffic Management Plan Automation (TMPA) solution under the 1Streetworks brand in the UK (1Streetworks).

IQGeo Group, down 0.7%, announced that Senior Vice President, Raf Meersman has been chosen as President of the Board of Directors at the FTTH Council. As Europe's leading fibre broadband industry organization, the FTTH Council mission is to accelerate ubiquitous full fibre broadband connectivity to empower the digital society of the future. Feedback, unchanged at 115.0p, today, in its trading update for the 12 months to 31 May 2023, announced that its trading performance has been in line with the Board’s and market expectations. Revenue for the period is expected to be around £1.0m (2022: £0.6m), up approximately 70%. As at 31 May 2023, cash and cash equivalents stood at approximately £7.3m (31 May 2022: £10.3m).

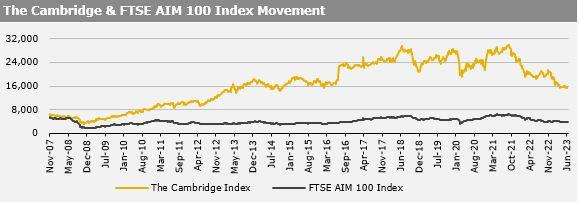

UK markets ended mostly higher last week, as Britain’s gross domestic product grew in April. On the macro front, UK’s economy rebounded in April, driven by robust growth in services sector, while the nation’s trade deficit narrowed in April. Additionally, the nation’s ILO unemployment rate dropped in the three months to April, while average earnings including bonus advanced more than forecasted in April. Meanwhile, UK’s industrial production fell more than expected in April, while the nation’s manufacturing production dropped more than expected in April. The FTSE 100 index advanced 1.1% to settle at 7,642.7, while the FTSE techMARK 100 index gained 1.8% to end at 6,851.6. Meanwhile, the FTSE AIM 100 index fell 0.2% to close at 3,780.3.

US markets ended higher in the previous week, after the US Federal Reserve (Fed) left its interest rate unchanged. On the macro front, the US retail sales advanced in May, following robust sales of motor vehicles and building materials, while the nation’s Philadelphia Fed manufacturing index declined less than expected in June. Also, the US Michigan consumer sentiment index rose to a four-month high in June. Meanwhile, the US consumer prices inflation rose at its slowest pace in May, reflecting a drop in energy costs, while the nation’s producer price index dropped more than expected in May. The US initial jobless claims remained unchanged in the week ended 09 June 2023. Separately, the US Federal Reserve kept its key interest rate unchanged at 5.25%, as expected. However, the central bank signalled that it would hike further interest rates by 50 basis points later this year. The DJIA index rose 1.2% to end at 34,299.1, while the NASDAQ index gained 3.2% to close at 13,689.6.