Sareum Holdings, up 2.6%, announced that that it has started an application to perform Phase 1 clinical studies on SDC-1801 in Australia under the Clinical Trial Notification (CTN) scheme. Documents required to initiate the trial under the CTN scheme have been submitted to a Human Research Ethics Committee (HREC) in Australia. A decision on approval by the HREC and acceptance of the CTN by Australia's medicines regulator, the Therapeutic Goods Administration (TGA), is expected in Q2 2023. Separately, the company announced that it would release its unaudited results for the six months ended 31 December 2022 on 22 March 2023. Science Group, up 0.8%, announced that it expects to release its preliminary results for the year ended 31 December 2022 on 21 March 2023.

GetBusy, down 4.7%, announced that it has no exposure to uninsured deposits and any loan facilities with Silicon Valley Bank (SVB).

IQGeo Group, down 3.8%, announced that that it would publish its results for the 12 months ended 31 December 2022 on 27 March 2023.

Oracle Power, down 2.9%, announced that its subsidiary, Oracle Energy, has entered into a Memorandum of Understanding (MoU) with Doosan Fuel Cell Co., Ltd and HyAxiom Inc. Under the MoU, the parties have agreed to jointly explore the fuel cell development opportunities for industrial power generation in Pakistan using green hydrogen to be supplied by Oracle Energy's Green Hydrogen Project. Today, the company announced that the recently acquired land lease of 7,000 acres has now been registered in the Government of Sindh's land registry.

CyanConnode Holdings, down 2.7%, in response to enquiries from shareholders, confirmed that it has no relationships with or banking arrangements involving Silicon Valley Bank (SVB).

Dialight, down 2.4%, announced that, in relation to the termination of their manufacturing services agreement with Sanmina Corporation, the court ruled against Sanmina's motion to dismiss Dialight's fraudulent inducement claim and denied its motion for summary judgment on Sanmina's accounts receivable claim.

Checkit, down 0.7%, announced that its exposure to Silicon Valley Bank was less than £0.1 million. Further, the company said it has a strong balance sheet, with net cash of £15.6 million as at 31 January 2023.

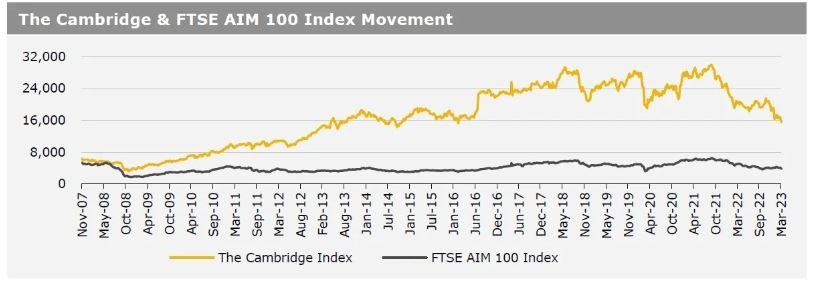

UK markets closed lower last week, amid broad sell-off in banking sector stocks. On data front, UK inflation expectations eased to a 16-month low in February. On the contrary, UK’s average earnings including bonuses advanced in January, while nation’s ILO unemployment rate remained steady in January. The FTSE 100 index declined 5.3% to settle at 7,335.4, while the FTSE AIM 100 index fell 4.6% to close at 3,815.9. Additionally, the FTSE techMARK 100 index lost 3.2% to end at 6,429.0

US markets ended mixed in the previous week. On the macro front, the US inflation slowed in February, while the nation’s retail sales dropped more than expected in February. Additionally, the US producer prices unexpectedly fell in February, indicating easing cost pressures, while the Michigan consumer sentiment index unexpectedly fell for the first time in four months in March. Moreover, the US industrial production recorded a flat reading in February, while the NY Empire State manufacturing index declined in March. Meanwhile, the US building permits and housing starts unexpectedly climbed in February, reflecting stability in the housing sector. In addition, the US weekly jobless claims dropped by most since July in the week ended 10 March 2023. The DJIA index fell 0.1% to end at 31,862.0, while the NASDAQ index gained 4.4% to close at 11,630.5.